Once pushed by rapid globalization and the expansion of Global Value Chains (GVCs), since the Great Trade Collapse of 2009, global trade has experienced a slowdown and entered a different phase, commonly called slowbalization. During this phase, the global geopolitical environment has become increasingly volatile. Shifting alliances, regional conflicts and great power competition, exacerbated by events like the US-China trade war, Brexit, the Covid-19 pandemic, energy insecurity and weakening multilateralism, have fundamentally altered the narrative and landscape of international economic relations. More recently, the Russian invasion of Ukraine, conflicts in the Middle East, China’s assertiveness in the Indo-Pacific and the transformation of US foreign policy have all contributed to a more fragmented and unpredictable world order and pushed governments and firms to rethink the configuration of production networks.

International trade has become a key arena of geopolitical contestation, and goods and capital flows are increasingly targeted on the grounds of national interests and geopolitical alliances rather than purely following economic interests and efficiency.

Nonetheless, amid rising concerns about deglobalization, trade and GVCs have shown unexpected resilience. GVCs, shaped by firm-level decisions facing high sunk costs, remain at the heart of global production, but are neither static nor unaware of the changing landscape. Aggregate trade data may suggest a peak or a plateau in globalization, but beneath the surface, trade patterns are increasingly fragmented and regionally driven. Rising geopolitical tensions, mainly based on sanctions, tech rivalry, energy security and national interests, are reshaping alliances and challenging the rules of global commerce.

This article explores how rising geopolitical tensions affect international trade patterns and GVCs. Rather than reversing globalization, we argue that a new phase is emerging, marked by re-globalization along geopolitical lines, where strategic alliances increasingly determine the direction of trade, investment and production, enhancing regionalization.

We first introduce the main themes and definitions characterizing the nexus between geopolitics and international economics, followed by stylized facts that illustrate the connections between economic developments and geopolitical shifts. We then discuss the future challenges facing firms and policymakers.

Geoeconomics: Politics and Globalization

Over the past two decades, the global narrative around trade and international production networks has undergone a profound transformation.

In the late 1990s and early 2000s, globalization was under scrutiny for its uneven socioeconomic impacts. While trade delivered aggregate gains, its distributional effects were leaving many behind, a concern that resonated beyond academic debates, manifesting in widespread public discontent and large-scale protests, such as those at the G8 summits in Seattle and Genoa, as well as in the mobilization of global civil society through initiatives like the World Social Forum. This growing scepticism toward globalization set the stage for a serious rupture: the 2008 Global Financial Crisis marked a decisive turning point, amid economic turmoil and rising public discontent. Governments, cautious of external shocks and under pressure to protect domestic jobs, began flirting with protectionist policies. Though economists urged caution and continued to advocate the benefits of open markets and multilateral cooperation, trade restrictions reappeared over time. The era of liberalization had ended; the trade narrative had begun to pivot toward a zero-sum game perspective.

This shift reached a symbolic peak in 2016 with the Brexit vote and played a key role in shaping the outcome of the US presidential election that same year. By 2018, the Trump administration had launched a trade war with China that extended beyond commerce, escalating geopolitical competition over technological dominance in key strategic sectors.

Between 2015 and 2019, the narrative around trade policy increasingly centred on import substitution. Protectionist measures were framed as necessary to address rising inequality, localized job losses were attributed to trade (often referred to as the “China shock”) and there was growing dissatisfaction with how globalization’s gains were distributed.

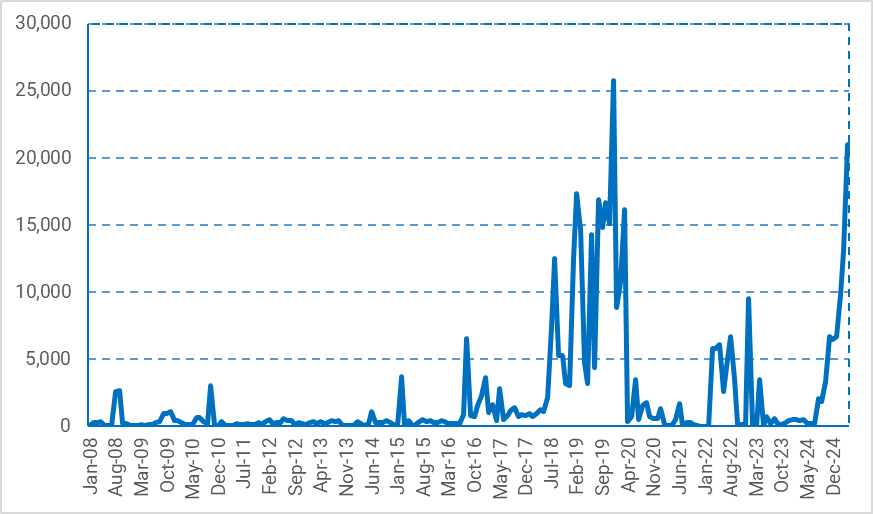

CHART 1 World Trade Uncertainty Index (Quarterly 2008-2024)

Then came Covid-19. The pandemic heightened global uncertainty (see Chart 1) and exposed the fragility of deeply interconnected supply chains, prompting a surge in protectionist sentiment. As governments rushed to secure critical medical supplies, export restrictions proliferated, even among close allies, demonstrating a shift toward inward-looking policies. This response, aimed at reassuring domestic electorates, reignited debates over the risks of global dependence and triggered calls to reshore production. Though international cooperation proved essential in mitigating shortages, the crisis nonetheless reinforced a narrative that favours national resilience over globalization, raising concerns about the long-term impact of these temporary but politically potent protectionist measures (Pinna & Lodi, 2021). In many ways, the pandemic accelerated and deepened a backlash against globalization that was already underway, particularly in advanced economies, where political movements and voters increasingly turned toward protectionist policies.

Russia’s invasion of Ukraine exposed the vulnerability

of global supply chains and the depth of strategic

dependencies in vital sectors such as energy,

raw materials and advanced technologies

The pandemic dramatically reframed the trade debate further. From 2020 to 2021, the focus shifted from import substitution to economic resilience. Shortages of medical supplies exposed the fragilities of global supply chains, prompting countries to impose export bans and reassess their dependence on foreign production. Policy discussions began to emphasize diversification, reshoring and reducing exposure to international shocks as strategies to strengthen national security and reinforce the robustness of global value chains.

While geopolitical undercurrents have long shaped trade relations, surfacing notably during the US–China trade war, they remained secondary to economic arguments. That changed abruptly on 24 February 2022, when Russia’s invasion of Ukraine pushed geopolitical risk to the top of the global agenda. This turning point exposed the vulnerability of global supply chains and the depth of strategic dependencies in vital sectors such as energy, raw materials and advanced technologies. Since then, the narrative around trade has adjusted once again, now centred on security, autonomy and de-risking, adding to the already existing uncertainty. Chart 1, which shows global trade-related uncertainty, highlights that the highest peak occurred during the pandemic. A similarly high level was almost reached again in the last two quarters of 2024.

Policymakers aimed to prioritize decoupling from rival powers by reinforcing economic ties within geopolitical blocs. Concepts like friendshoring have taken root, where countries shift production and sourcing toward trusted partners to reduce exposure to hostile or unstable actors. This shift has also been accompanied by a resurgence of industrial policy, with governments rolling out initiatives to bolster domestic industries, enhance technological sovereignty and reduce reliance on foreign inputs.

The rise in geopolitical conflicts has brought renewed attention to economic sanctions as key instruments for penalizing aggressive states. Beyond being visible responses, sanctions signal a broader shift in which geopolitics increasingly influences firm behaviour, investment decisions and global economic planning. Unlike tariffs, which protect domestic markets, sanctions aim to exert geopolitical pressure, often triggering trade disruption, countersanctions and systemic instability. Their use, especially multilaterally, has surged in recent decades. Since 2022, EU sanctions alone have impacted over half of Russia’s trade, contributing to a projected long-term GDP loss exceeding 10%. Sanctions now significantly affect global value chains, reducing participation in targeted countries and accelerating GVC fragmentation and realignment.

Empirical research (summarized in Giovannetti et al., 2025) has shown that trade between geopolitically aligned countries is significantly more robust. According to recent estimates, trade within geopolitical blocs has grown 4–6% faster than trade between different geopolitical blocs (IMF, 2025). WTO claims that a 100 percent increase in tariffs between two hypothetical geoeconomic blocs, combined with increased uncertainty in trade policies and increased non-tariff barriers, will reduce global real GDP by nearly seven percent in the long run (by 2040). Low-income economies are the hardest hit, with losses exceeding nine percent. Moreover, starting in 2018, geopolitical distance has emerged as a statistically significant barrier to bilateral trade, particularly in manufacturing. This effect compounds traditional frictions such as geographical distance and tariffs, signaling a shift toward geo-economic fragmentation.

Geography and Geopolitics of GVCs: Stylized Facts

Geopolitical relationships play a role in shaping global trade and investment. While aggregate globalization metrics, such as trade-to-GDP ratios, remain relatively stable, deeper currents reveal a reorientation of economic linkages along geopolitical lines. Since the war in Ukraine, trade, foreign direct investment (FDI) and capital flows between countries in opposing geopolitical blocs have declined significantly. On the other hand, flows within aligned blocks have remained more resilient. This growing fragmentation is not driven solely by economic fundamentals, but by strategic concerns around national security, technological sovereignty and supply chain resilience. Unlike the Cold War era, however, today’s landscape includes economically integrated connector countries that maintain links across blocs and may buffer some of the disruptive impacts of fragmentation. These shifts suggest a changing geography of globalization, where the choice of trade and investment partners is becoming more affected not just by economic cost or proximity, but also by barriers and/or facilitation due to international politics (Gopinath et al., 2025).

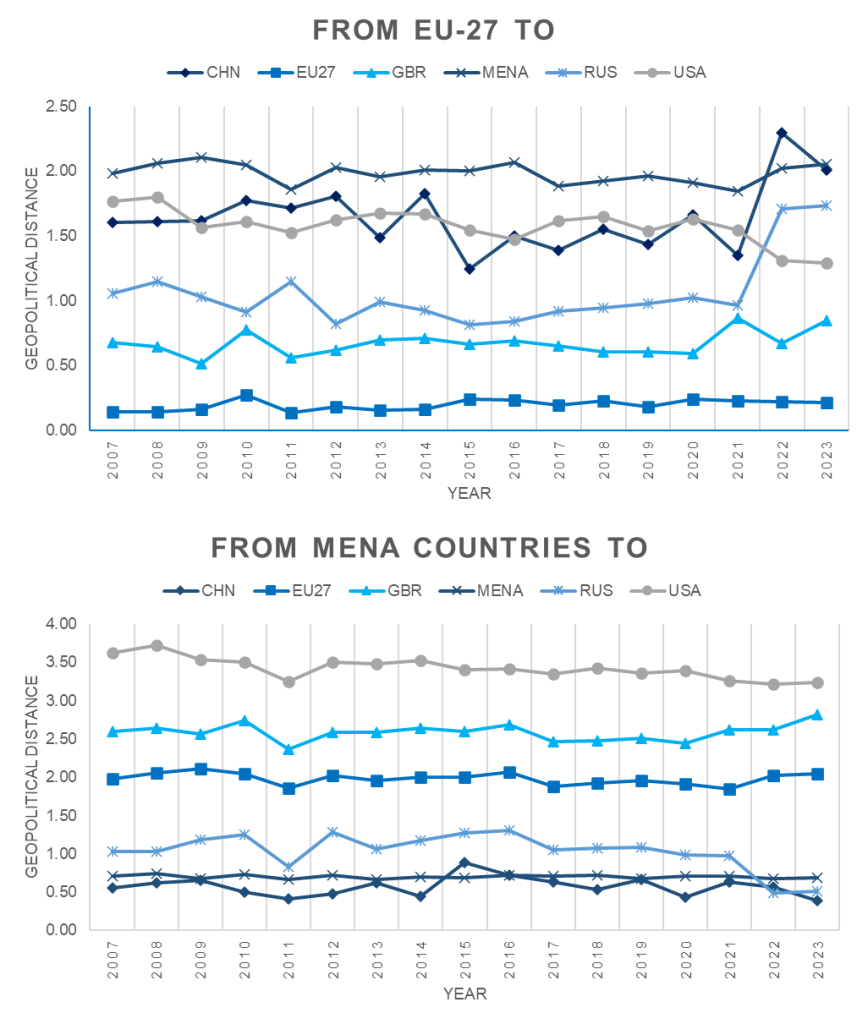

A commonly used measure of geopolitical distance is the ideal point distance derived from the United Nations General Assembly (UNGA) voting records. Chart 2 illustrates the evolution between 2007 and 2023 of geopolitical distance from EU-27 (top panel) and Middle Eastern and North African countries (MENA) (bottom panel) to relevant global actors in international geopolitics. The overall trend suggests growing geopolitical fragmentation and realignment, especially after major events such as the 2014 annexation of Crimea and the 2022 full-scale invasion of Ukraine.

In the EU-27 panel (top), geopolitical distance with Russia increases steadily, especially after 2022, reflecting growing divergence and strategic decoupling. EU’s geopolitical distance with China has increased recently, whereas ties with long-standing partners like the US and UK have remained consistent (data refer to before Trump’s “liberation day” announcement of tariffs that would also affect “friends”). The EU-UK geopolitical distance slightly increases in two moments: the first is in 2010, when in Great Britain the government was formed by a Conservative-Liberal coalition, and this period stands between the end of the Iraq War and the civil conflict in Libya; the second is in 2021, and is probably related to Brexit negotiations. The most distant country group from the EU is the MENA bloc. A geopolitical fracture between the EU and China emerges in the second wave of the Covid-19 pandemic. Distance within the EU-27 group (the simple average distance between Member States) remains very low and flat between 2007 and 2023. Despite internal discussions, this indicates a strong and enduring internal cohesion, reinforcing the EU’s role as a relatively unified geopolitical actor amid external turbulence.

In contrast, the MENA panel (bottom) reveals a more heterogeneous landscape. This region is relatively distant from the EU, but even less aligned with the US and UK. The geopolitical distance to the US starts high and slowly declines, indicating a slight convergence. Distances to Russia and China remain low and relatively stable, possibly reflecting deeper or more flexible diplomatic ties. In particular, the alignment between MENA countries and Russia, on average, weakened after the pandemic and during the Ukrainian invasion. Importantly, within-group distance among MENA countries (MENA–MENA) is significantly higher than among EU members and shows a modest but persistent decline. Hence, while regional alignment in the MENA region has improved marginally over time, intra-group political cohesion remains relatively weak, highlighting internal fragmentation and diverging foreign policy orientations within the area.

CHART 2 Geopolitical Distance by Pairs over Time (2007-2023)

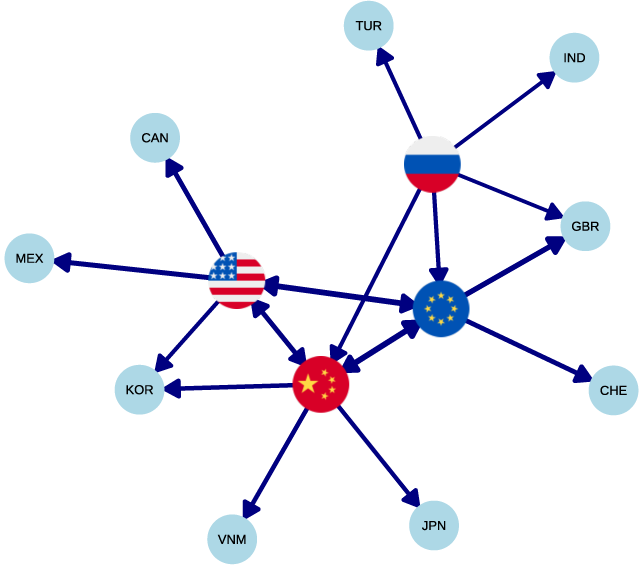

CHART 3 GVC Exports in Manufacturing by Selected Countries – Top 5 Flows 2022

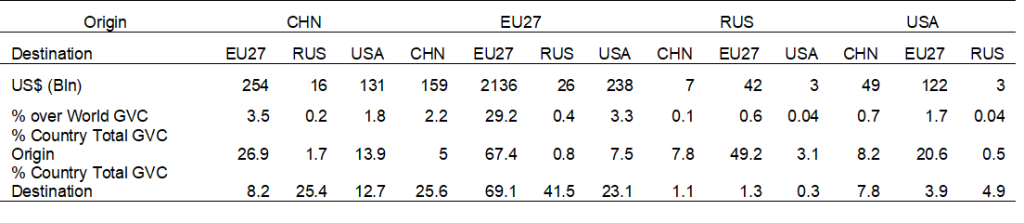

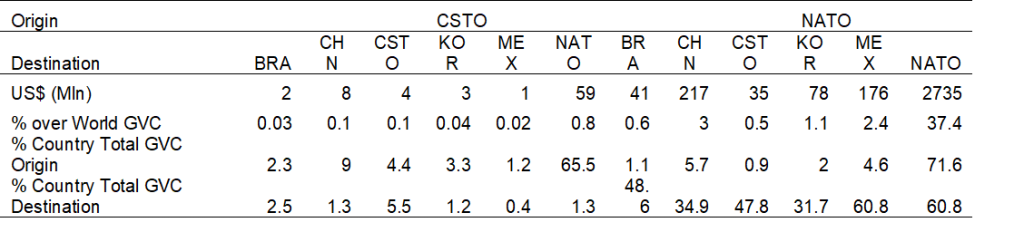

TABLE 1 GVC in Manufacturing – Top Flows in 2022: Values and Shares by Country

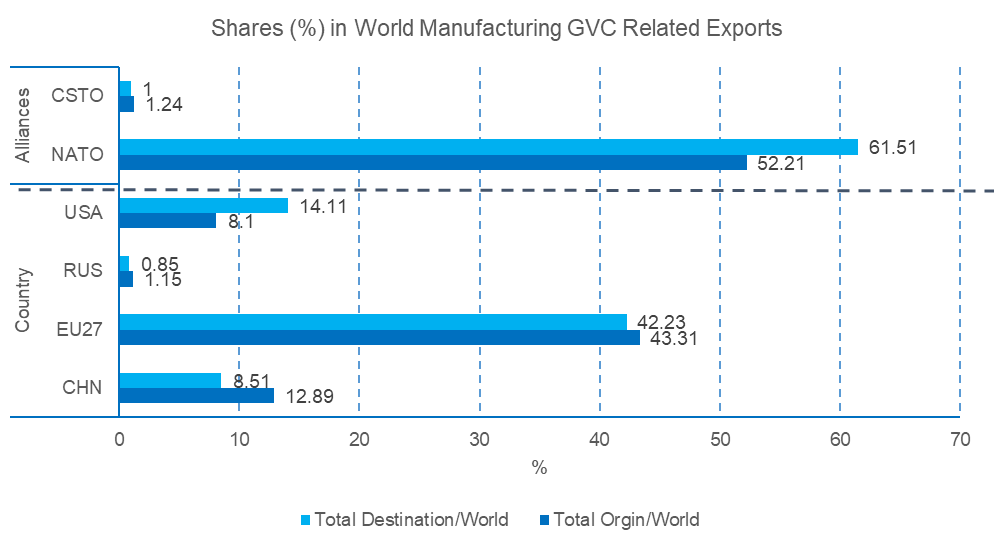

Chart 2 highlights how global manufacturing remains deeply interconnected, even as geopolitics increasingly shapes trade flows. The United States, China and the European Union stand out as the main hubs, all accounting for over 60% of global value chain (GVC) activity in manufacturing (see Chart 5). Even as political tensions rise, these powerful economies keep trading with each other, showing how closely linked they still are.

For example, in 2022, China sent over $250 billion in manufacturing exports to the EU and over $130 billion to the US. The EU, in turn, exported nearly $160 billion to the US and an even larger $2.1 trillion to China (see Table 1). Meanwhile, the US maintained significant manufacturing ties with both partners. These dense trade links underline the resilience of global production networks, even amid geopolitical strain.

Beyond the big three, countries like Japan, South Korea and Vietnam are critical bridges in Asia, connecting Western and Eastern production systems. Others, like Mexico, India and Turkey, play important regional roles, though with fewer global connections. Russia’s export pattern, in contrast, has shifted sharply toward China and away from the West, reflecting the growing impact of sanctions and strategic decoupling.

CHART 4 GVC Exports in Manufacturing from Military Alliances (groups of countries) to Main Partners – Top 10 Flows 2022

TABLE 2. GVC in Manufacturing – Top Flows in 2022: Values and Shares by Military Alliances

Military alliances can also shape global trade (see Chart 4), especially in manufacturing. NATO stands out not just as a security alliance, but also as a major economic force (since its members represent a relevant fraction of world GVC-related trade in manufacturing, see Chart 5). In 2022, NATO countries exported nearly $2.73 trillion (see Table 2) in manufacturing goods to fellow members and large amounts to key partners like China, Mexico, South Korea and Brazil, emphasizing their central role in global value chains. By contrast, the CSTO, led by Russia, plays a much smaller role in global manufacturing trade (see Chart 5 and Table 2). Its exports are modest and heavily dependent on trade with NATO countries, reflecting weaker industrial capacity and limited global reach, even if its members are also geographically close.

As trade becomes more entangled with strategic concerns, alliances like NATO are relevant as political and economic blocs. Their members form a tightly connected trade network, particularly in high-value manufacturing. While some countries like Japan, South Korea and Mexico trade with both sides, the overall picture shows NATO-aligned economies dominating the global manufacturing landscape.

Chart 5 World GVC Manufacturing Participation, Selected Countries and Military Alliances

The data in Tables 1 and 2 underline the geopolitical asymmetries in GVC participation, with NATO countries (especially the US and EU27) and China dominating both as sources and destinations of value-added trade. This reflects their strong industrial bases, political stability and capacity to meet international standards. In contrast, countries aligned with CSTO, including Russia, show marginal GVC involvement, highlighting the limited integration of these states into high-value segments of global production. Moreover, these patterns suggest that participation in GVCs is not only about geography or resources but also hinges on institutional quality, certification standards and the ability to meet buyers’ expectations. The work of Del Prete et al. (2017) provides evidence from North Africa, indicating that countries can improve their geopolitical and economic standing by deepening GVC participation, enhancing firm-level productivity and international certification compliance. Therefore, GVCs are not just economic phenomena but also strategic instruments that reflect and reinforce global power dynamics.

GVCs are not just economic

phenomena but also strategic

instruments that reflect and

reinforce global power dynamics

Conclusion: Summary and Future Perspectives

Despite recent shifts toward protectionism – clearly reflected in events like Brexit, the US-China trade war and pandemic-era export restrictions – global trade and value chains have demonstrated remarkable resilience. Trade-restrictive policies have reduced trade flows and raised costs, especially for the countries imposing them, but have not reversed globalization. Instead, global production networks have adapted, often through reconfiguration rather than retreat. The evidence suggests that while temporary shocks, such as Covid-19, have triggered short-term disruptions, they have not led to structural reshoring. However, continuous shifts in political narratives related to geopolitics, national security and industrial policy could drive longer-term transformations in trade and GVC architecture.

In today’s complex and uncertain environment, businesses of all sizes and policymakers at every level must manage emerging risks while seizing strategic opportunities to rethink and reshape global trade and production networks.

Policymakers must navigate a delicate balance between enhancing resilience and preserving efficiency in global trade networks. As geopolitical risks grow, there is increasing pressure to shift trade toward aligned partners; yet doing so may inadvertently heighten supply chain concentration and reduce economic flexibility. To reduce risk, it is essential to pursue strategic diversification across both geographic and political lines, especially for those sectors that depend on a limited number of suppliers. Policymakers should also leverage trade and foreign investment to build long-term strategic alliances. In particular, they could seek to expand partnerships with emerging markets such as India, ASEAN nations, Latin America and parts of Africa (McKinsey Global Institute, 2024).

It will be crucial to coordinate domestic, international and multilateral policies. At the firm level, governments can encourage industry to strengthen scenario planning and prepare for geopolitical disruptions, especially in sectors exposed to critical or politically sensitive inputs. As far as the multilateral level is concerned, a coordinated global trading system remains vital to counter rising fragmentation and safeguard openness. Focusing on the Mediterranean region, where integration into global value chains remains uneven, there is a pressing need for regional cooperation and industrial upgrading. While northern Mediterranean countries play key roles in advanced manufacturing, their southern and eastern neighbours often remain confined to lower-value-added segments. To address this gap, coordinated policies, through platforms like the Union for the Mediterranean, should aim to elevate industrial capacity, improve alignment with international standards and capitalize on the region’s geographic proximity to Europe and Africa. Finally, this would position Mediterranean economies as resilient, strategic hubs in a shifting global trade landscape.

References

Del Prete, Davide; Giovannetti, Giorgia; Marvasi, Enrico. “Global value chains participation and productivity gains for North African firms.” in Review of World Economics, n. 153(4): 675–701, 2017.

Giovannetti, Giorgia; Lodi, Luca; Marvasi, Enrico. “Global value chains under geopolitical distress.” In Cipollina, Maria, Randolph, Luca, Reshaping Global Value Chains: Approaches and Insights from Economics. Cambridge: Cambridge University Press, 2025 (Forthcoming).

Gopinath, Gita; Gourinchas, Pierre-Olivier; Presbitero, Andrea F.; Topalova, Petia. “Changing global linkages: A new Cold War?” in Journal of International Economics, n. 153: 104042, 2025.

IMF, World Economic Outlook, Chapter 1, April 2025

McKinsey Global Institute. Geopolitics and the geometry of global trade. McKinsey & Company, 2024.

Pinna, Anna Maria; Lodi, Luca. “Trade and global value chains at the time of COVID-19.” in The International Spectator, n. 56(1): 92–110, 2021.

Header Photo: The APMT container terminal in Barcelona and the cruise terminals at Adossat Wharf. Photo: Port of Barcelona