The Mediterranean Solar Plan as a Euro-Mediterranean vector of Integration and Economic Development

Introduction: Renewable Energies and the Union for the Mediterranean

Energy scenarios predict a rapid expansion of renewable energies worldwide. By 2015 (2030) the International Energy Agency estimates 678 TWh (1,535 TWh) of wind generation and 67 TWh (402 TWh) of solar origin (IEA, 2009). Much of this potential is concentrated in the EU Mediterranean neighbourhood, which in its turn is one of the most active actors in renewable energies internationally. However, without including hydroelectricity, the contribution of renewable energies in southern and eastern Mediterranean countries is still very low. OME estimates (2008) indicate that it will pass from an annual production of 2 TWh in 2005 to 33 TWh in 2020, while in the north it would pass from 51 TWh in 2005 to 96 TWh in 2020; production capacity in 2020 would be 73 GW in the north and 14 GW in the Mediterranean partners. In other words, in the base scenario, the rate of development of renewable energies in the south is very high. Nevertheless, most of the region’s capacity will continue to be installed in the EU.

Moreover, the projections for growth in demand for energy, and especially electricity, in the EU Mediterranean neighbourhood until 2020 are very high. According to the OME, energy demand would grow by 4.8% annually and electricity demand by 6%; to supply this, it would be necessary to install an additional 106 GW and double the annual production from 500 to 1,000 TWh. Despite this growth, the consumption per capita of electricity in the south and east would go from around 1,800 kWh in 2005 to almost 3,100 kWh in 2020. That is, the acute demographic growth, together with urbanisation and industrialisation, would absorb much of the increased capacity. In this scenario, the electricity consumption per capita would stay far below the consumption of the north, estimated at around 6,500 kWh in 2005 and 8,800 kWh in 2020. These differences illustrate the potential growth in demand for electricity in the southern and eastern Mediterranean as the population rises, the urban middle classes adopt new consumption habits, and the rural areas gain access to modern energy services.

In this context, one of the six projects included in the annex of the Paris Declaration of 13th July 2008 formally establishing the UfM[1] is the so-called “Alternative Energies: Mediterranean Solar Plan”. The final objective of the Mediterranean Solar Plan is to develop an additional 20 GW of renewable capacity by 2020. Despite its denomination, the meaning of the Declaration calls for the mobilisation of all alternative energies, also later emphasising energy efficiency. The spirit that inspires the UfM is to accompany the commercial integration of the Euro-Mediterranean Partnership and the regulatory convergence implicit in the European Neighbourhood Policy with physical integration through structuring and unifying projects in the Euro-Mediterranean region.

The Mediterranean Solar Plan provides several opportunities for Euro-Mediterranean cooperation. On the one hand, the EU aspires to world leadership in renewable energies, as they are a base element of European energy policy.[2] Their development has become one of the signs of identity of the Community energy policy and, after the approval of the 20/20 commitment, a necessity to achieve the objectives of the new Directive 2009/28 on the promotion of the use of energy from renewable sources. The Commission has recognised that for some countries it can be difficult to achieve the objectives set, but the new directive allows, under certain circumstances, a Member State to transfer its surplus renewable energy to another that has not reached its objectives, as well as to establish cooperation mechanisms with third countries. The geography and the climatic conditions mean that the greatest potential of the European neighbourhood in terms of the development of renewable energies is in the southern Mediterranean.

On the other hand, the Mediterranean Partner Countries (MPCs) have shown interest in exploiting their wind and solar potential, both to confront their growing energy demands and to export electricity from renewable sources to the EU. For the MPCs, the development of renewable energies has an interesting socioeconomic potential. Renewable energies can stimulate their economies through the promotion of Foreign Direct Investment, the generation of new local energy sources, the export of renewable energy to the EU, job creation and encouraging R&D and technology transfer, which can entail the delocalisation of certain industrial processes, such as the manufacture and assembly of components in the wind or solar industry. In those countries without hydrocarbons, renewable energies can be a medium and long-term solution to reduce their economic and energy vulnerability. In certain circumstances, their development could be an additional motor of development for the EU Mediterranean neighbourhood.

These shared interests explain the attention received by the Solar Plan. Among other vectors of cooperation, the Solar Plan offers the double opportunity of expanding Euro-Mediterranean integration and accompanying the economic development of the MPCs, as long as a series of current limitations are dealt with. However, for this it is necessary from the outset to approach the Mediterranean Solar Plan itself as a cooperation programme to foster the development of the MPCs and Euro-Mediterranean integration, considering its connection with the broadest institutional framework of the UfM and the European Neighbourhood Policy. To the extent that the integration of renewable energies entails an adaptation to the institutional and regulatory framework, their encouragement is also a factor of modernisation of the energy systems. But these reforms involve a certain regulatory convergence to make regional integration possible, at least electricity, both at a Euro-Mediterranean and South-South level. This integration, moreover, is consistent with the logic of the comparative advantage, as it allows the MPCs to exploit abundant obsolete factors, such as desert areas and hours of insolation.

Moreover, in the Euro-Mediterranean scenario there are other energy elements of great immediate importance, such as hydrocarbons, and the role of renewable energies cannot be detached from the global energy mix and its geo-economic implications. Many of the arguments used for renewable energies, such as improvement and harmonisation of energy regulation or the need to undertake the installation of new generation and transport capacities, can be extrapolated to the whole energy system. In a sense, the renewable energies sector can be a good candidate to begin a process of Euro-Mediterranean regulatory harmonisation and convergence, which could have overflow effects on the other sectors. It is a new sector, relatively small and more open to regulatory innovations which can then be studied for their application to other kinds of energy, for example grid energies such as electricity or natural gas.

However, the mass development of renewable energies continues to pose some uncertainties. Firstly, the estimated costs are high, especially in the current economic context. The initial French-German position on the Mediterranean Solar Plan of August 2008 put forward the amount of €80,000 million, which has remained as the reference; but other estimates point to a bracket between €38,000 million (Lafitte et al., 2009) and €97,000 million (Estela Solar, 2009), which means a high dispersion of figures. Currently, the REACCESS project of the 7th EU Framework Programme is carrying out an optimised estimate of the different EU energy corridors that will produce more detailed cost estimates, but the results will not be available until the end of the project. However, it is important to play down these amounts in the context of the energy needs of the MPCs: the OME (2008) estimates that investments as a whole in the electricity sector of the MPCs until 2020 is €320,000 million, including generation, transmission and distribution installations.

Furthermore, renewable energies still require a transitional support to advance in the learning curve until reaching the competitiveness threshold. They also need a stable institutional context that reduces the regulatory risk and allows investments involved in their high capital intensity, generating the right conditions to establish a sustainable framework in the long term for their development. The analysis of the incentive and legal measures adopted by the MPCs in renewable energies shows some progress, but at different rates. In many of them legal and institutional barriers persist, also at an infrastructure level. All these elements should benefit from technical cooperation and training programmes to improve the legal framework and give the regulatory bodies and administration greater analysis and supervision skills.

In short, the Mediterranean Solar Plan poses uncertainties in terms of the kind of technologies, the number and the capacity of the generation installations, the transmission of electricity generated with renewable energies, the need or otherwise for complementary projects, the regulation schemes to be applied and the funding mechanisms, among others. The scope of the challenges to be faced requires careful consideration, as without a realistic approach and the implementation of operating measures to ensure the feasibility of the project, its credibility will continue to be in doubt (Benavides, 2010).

This document seeks to stimulate discussion about the Mediterranean Solar Plan project, offering a basis for reflection on the conditions under which, at least partly, these obstacles could be overcome and make the Solar Plan an instrument for Euro-Mediterranean integration and the development of the MPCs. To this end, we firstly summarise the state of the issue in terms of the identification of projects to be undertaken, their funding and their regulatory framework. Secondly, we analyse the Mediterranean Solar Plan as a vector of integration, with special attention to the implications of Directive 2009/28 and the applicability of the Energy Community Treaty model. The third section explores the role of renewable energies as a vector of sustainable development in the Mediterranean and the need to improve the absorption capacity of the MPCs through training, technical cooperation and technological cooperation for development programmes.

The Mediterranean Solar Plan: Progress in the Identification, Regulation and Funding of Projects

The annex of the Paris Declaration “Alternative Energies: Mediterranean Solar Plan” confirms the need to focus on alternative energies and estimates that “market development as well as research and development of all alternative sources of energy are therefore a major priority in efforts towards assuring sustainable development.” Under the French-Egyptian Co-Presidency the adoption of an “Immediate Action Plan 2009-2010” to develop concrete projects was proposed. Its objectives were to advance in the learning curve, organise efficient governance in the MPCs, and involve public and private actors. It also proposed the setting up of several projects to allow the countries involved to test their respective regulatory frameworks and define new funding schemes and electricity exports generated by renewable energies towards the EU. The criteria established for the selection of projects was the capacity to start them in 2009-2010, the existence of an industrial sponsor and the commitment of the host country to ensure the commercial feasibility of the project.

| Box 1: Antecedents of the UfM: The Barcelona Conference and the European Neighbourhood Policy The 1995 Barcelona Conference established the bases of a Euro-Mediterranean Partnership whose objective was to achieve shared peace and prosperity in the region. The Partnership was structured around three baskets: economic, political and security, and culture, to which was later added the dimension of justice and home affairs. Within the economic basket, actions have consisted of establishing a Euro-Mediterranean free trade area through bilateral agreements with the MPCs, economic cooperation and financial cooperation. This framework has resulted in the cooperation to achieve the Mediterranean Energy Ring (gas and electricity). The UfM incorporates the whole of the Barcelona acquis but gives it a new governance. In 2003, the European Commission launched the Neighbourhood Policy, based on offering neighbouring countries participation in different aspects of the Single European Market if they demonstrated their convergence with the respective Community acquis: “all except the institutions,” in Romano Prodi’s words. Neighbourhood Action Plans were agreed that involved the selective adoption of the Community acquis, including the energy sector. On 7th March 2010, in Granada the first EU-Morocco Summit took place, as set out by the Advanced Statute with this country, which means closer relations and, also, considerations about energy and, specifically, the promotion of renewable energies. Finally, the Paris Declaration of 13th July 2008 formally established the UfM, which inherits the Euro-Mediterranean Partnership acquis and adds to it a series of structuring projects, including the Mediterranean Solar Plan, as well as a new governance of the process, based on the co-presidencies and on the creation of a UfM Secretariat, based in Barcelona and whose statutes were approved, after long discussions, in February 2010. |

The France-Egypt Co-Presidency proposed the creation of a technical group with representatives from several Euro-Mediterranean countries with the aim of carrying out the selection of these projects and discussing the preparation of other action plans. It was also proposed to work with the multilateral financial institutions to design a funding scheme to facilitate these kinds of projects. In parallel to the application of the “Immediate Action Plan 2009-2010” this task force was responsible for preparing a Master Plan 2011-2020. The Roadmap designed, made up of the immediate and master plans, has been normalised with the cooperation of a core of countries: Germany, Spain, Italy and France from Europe, and Morocco and Egypt from the MPCs. In the energy ministerial meeting in June 2009, two documents were produced: a strategic document and another about the governance of the process.

Apart from the institutional developments, to date the discussion about the Mediterranean Solar Plan has basically focused on the types of projects to be selected, their funding and the regulation of Community electricity exports from renewable installations in the MPCs. Before attempting to widen the focus of the discussion to aspects related to regional integration and the economic development of the MPCs, the rest of this section is dedicated to revising the discussion about the three aforementioned aspects.

An Advanced Process in Terms of Project Identification

In recent years, there have been numerous analyses of the potential of renewable energies (basically solar and wind) in the southern Mediterranean. Box 2 summarises the main initiatives recommended by these studies. Without assessing the methodologies or the assumptions adopted for their preparation, many of them coincide in the types of projects to be undertaken, have been tested with public and private actors, and are the existing starting point for UfM renewable energy projects, when they do not directly inspire them.

| Box 2: Tentative identification of projects in the Mediterranean Installation of renewable electricity generation capacities in the MPCsMPC-EU construction of high-capacity HVDC lines Improvement of electricity grid of the MPCs and intra-regional interconnections Natural gas capacities in MPCs to supplement renewable energiesDesalination plan through renewable energies Energy efficiency projects Sources: DLR (2005), European Commission (2007), OME (2007 and 2008), Plan Bleu (2007, 2008a, b), REACCESS-DLR (2009), REACCESS-UNED (2009), TREC (2007a), RaL (2007), ESTELA (2009), PWC (2010), (MED-EMIP, 2010). |

Renewable energy installations

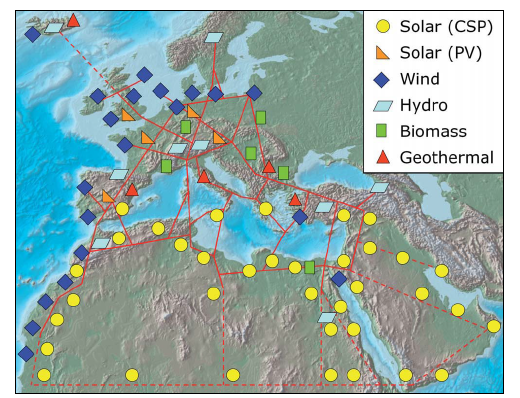

The potential of the renewable energies in the region is quite well established, and is summarised in a simplified way in Map 1, which also presents an estimate of the electricity corridors necessary for transmission of the electricity generated to the EU and between the MPCs themselves. In principle, the greatest potential is found in solar energy but the wind potential is also very important on the Atlantic coast of Morocco, as well as in Egypt and Turkey, and in numerous locations in the south of the Mediterranean (although infra-represented on the map). Hydraulic energy has potential in Egypt and Turkey (in both cases for large dams) and in Morocco (for small dams).

The first question lies in identifying the optimum technological options. Lafitte et al. (2009) pose four alternative scenarios: two extreme scenarios, one exclusively solar and another wind; and two more probable hybrid scenarios, the ‘solar +’, predominantly solar (5.2 GW photovoltaic, 7.8 GW of CSP and 7 GW wind); and the ‘wind +’, predominantly wind (13 GW wind, 3.1 GW photovoltaic and 3.9 GW of CSP).

The figures supplied by ESTELA (2009, p. 6), the European Solar Thermo Electricity Association, which only considers the region of North Africa, are much higher. According to the estimates, the electricity generation through CSP in this region could reach 32 TWh/year in 2020 and 286 TWh/year in 2030. Despite only representing a tiny fraction of the available technical potential, the figures for 2030 are much higher than those projected for Europe, for which ESTELA establishes the potential at 90 TWh/year for 2020 and 195 TWh/year for 2030. According to these same estimates, in 2020 the CSP would represent 3% of Euro-Mediterranean electricity consumption, and would rise in 2030 to 10.6%. In 2030, therefore, around 7% of the electricity consumed in the region would originate in the CSP generated in installations in North Africa. In 2030, around 6% of European electricity imports would come from CSP installations in North Africa.

Map 1. Renewable energies and electricity corridors (HVDC) in the Euro-Mediterranean space

Photovoltaic energy can also be developed in some of the locations established for the CSP, as the option of implementing one technology or another can depend on factors such as the evolution of total costs or technology maturity. In fact, photovoltaic solar energy has an important effect on rural electrification in southern Algeria, in some areas of Egypt and, above all, in the Moroccan rural electrification programme. Photovoltaic energy also has an important role to play in decentralised installations and isolated population centres, circumstances of special interest in many MPCs. In the scenarios outlined by Lafitte et al. (2009) for 2020, photovoltaic energy would contribute with a capacity between 3.1 GW and 5.2 GW in the hybrid wind and solar scenarios, respectively.

The wind potential is very high in determined countries, such as Morocco, Egypt or Turkey, but it is also notable for specific locations on the coast in the remaining southern and eastern Mediterranean basin. In a wind scenario, it would account for 65% of the 20 GW of the installed capacity in 2020, and for 35% in the solar scenario. However, despite the advances made in the three aforementioned countries, at present wind energy represents a marginal contribution in the region as a whole. The onshore wind technology has the advantage of having lower investment costs and being closer to the profitability threshold and, therefore, the generation would tend to give priority to onshore technology in the early phases of the Mediterranean Solar Plan.[3] However, offshore wind energy also has a great potential in the region and several advantages over the onshore, although it is still faced with technical problems (IEA, 2008a). Thus, there is nothing in the design of the Plan (apart from its name) or in Article 9 of Directive 2009/28 which represents any obstacle for its application to wind energy. Moreover, the IEA (2009) estimates that it will soon become in the second source of renewable energy, only behind hydroelectricity, reaching 4.5% of world electricity generation in 2030 and 8% in the OECD.

Table 1: Cost estimate for selected renewable energies: Strong dispersion and uncertainty over future evolution

| Technology | Investment (€/kW) | Cost (c€/kWh) |

| Wind Onshore Offshore | 1100-1300 2200-2400 | 4-8 6-10 |

| CSP | 3000-4000 | 15-23 |

| Photovoltaic On grid Isolated | 3000-6000 7000-12000 | 20-40 40-100 |

| Gas combined cycle | 350-650 | 6-8 |

| Coal plant | 1200-1400 | 4-6 |

Source: Resources and Logistics-RaL (2010), table 8, p. 38.

The cost estimate compiled by RaL (2010) in its report for the European Commission is presented in table 1.[4] It can be seen that wind technology currently shows competitive costs with gas or coal in regions with many wind hours and speeds. The rapid decrease of the photovoltaic technology costs suggests that it can achieve parity with grid prices in the next few years, especially in a context of high electricity prices. Moreover, most studies carried out indicate that solar thermal energy can only be competitive in the medium term and contribute to the reduction of conventional generation costs (TREC, 2007a, p. 37). The TREC study concludes that electricity from CSP imported from North Africa will in 2020 be 25-30% cheaper than that produced in southern Europe.

The Mediterranean Solar Plan therefore poses the initial dilemma over which technological option should be prioritised. Solar thermal technology has only been developed in the southern Mediterranean on a small scale, mainly two hybrid plants with combined cycle power plants in Algeria and Morocco. A short-term option would be to support new projects that demonstrate this technology in order to promote it in the medium and long term when its technology maturity permits more precise regulatory decisions. Wind generation seems closer to the profitability threshold and there is an important potential in Morocco, Algeria, Egypt and Turkey. For its part, photovoltaic energy has great potential in the rural environment, as well as in large and medium sized decentralised installations, and it would be advisable to include it in the projects for selection. Moreover, the installation of CSP in areas with greatest insolation should also be carefully considered in order to achieve scale economies and help cost reduction.

In any case, the mere identification of a major potential for solar and wind renewable energies in the region is only the first step in the reflection on the exploitation and integration of these resources by the EU and the MPCs themselves. There are other projects envisaged by the literature that mean that the Mediterranean Solar Plan must be considered globally.

Transmission lines, grid improvements, support capacities and desalination

First, export of electricity generated through renewable energies to European markets requires transmission routes from the future installations in the south. At present, only the Maghreb is interconnected with the Community electricity market in a synchronised and continuous way, albeit modestly, through the Spain-Morocco interconnection. The underwater link between Spain and Morocco has two cables of 700 MW, so that in the short term the Mediterranean Solar Plan installations aimed at the export of electricity can only be developed in the Maghreb, basically in Morocco, with a theoretical capacity limited to 1,400 MW. Map 1 also illustrates the trans-Mediterranean electricity corridors considered optimal to allow the transmission of electricity generated through renewable energies to the EU (TREC, 2007a):

- Extension of the existing Morocco-Spain connection

- Algeria-Spain direct connection

- Algeria-North Italy connection

- Tunisia-Italy (North and South) connections

- Libya-Italy and Libya-Greece connection

- Egypt-Turkey-EU connection

The studies advocate the creation of a High Voltage Direct Current (HVDC) grid, a supergrid to carry the energy generated in the MPCs to the EU. In the longer term, some studies indicate the need for a supersmart grid for greater expansion of renewable energies in the Euro-Mediterranean region (PWC, 2010). Perhaps the biggest problem is the demanding and fragmented approval procedures for this type of infrastructure in the EU and its Member States. Given its nature, it is delayed by the national and, on occasions, regional and local procedures. Thus, the new EU Energy Security and Infrastructure Instrument should include measures to guarantee interconnections within appropriate timeframes. The EU should be able to intervene – whether through domestic market legislation, other pertinent legislation, or funding – in cases of failure of regional or private initiatives. It would therefore be necessary to have mechanisms within the Treaty and the derived legislation to resolve cases of inaction in the development of absent or deficient capacity links in the Trans-European Energy Networks.

Alternatively, the development of the technology of underwater power lines can help palliate some of these obstacles. Another key element lies in establishing the role of the localutilities, highly familiar with the national and local procedures and rules, as a support for the development of infrastructures, both in the southern and northern Mediterranean, thus facilitating the promotion and invigoration of these infrastructures and their integration into the socioeconomic environment.

The second element necessary to develop renewable energies in the southern and eastern Mediterranean is the improvement and modernisation of their electricity grid. The fact of connecting with the EU and between the MPCs themselves strengthens their systems, but it demands an effort to modernise them. A significant increase in the contribution of renewable energies means a challenge of additional improvement for their system, given that renewable energies require major grid capacities and their integration into it presents additional problems of managing supply and demand. But this strengthening is not limited to the MPCs. The connection of an HVDC line between southern Mediterranean countries and EU Member States to export large amounts of electricity would also mean the need to strengthen the electricity grid of southern Europe to avoid congestion. Moreover, access to renewable energy installations in countries without direct connections with the EU to the Community electricity market (the cases of Libya or Egypt) requires specific projects to improve sub-regional interconnections. The development of the Mediterranean Electricity Ring is an equally important challenge, especially bearing in mind the limited progress made to date (MED-EMIP, 2010).

Another important aspect is that the integration of renewable energies demands greater flexibility from the system to manage it adequately, for which there are related mechanisms, such as the relaxation of natural gas supply contracts, which should include the take or pay clauses. In fact, most of the studies note that the gradual entry in operation of renewable energy installations can require greater support capacities based on natural gas, specifically in combined cycle power plants that can supply the peaks in demand. These scenarios indicate that renewable energies will achieve 25% of the OECD electricity generation, surpassing natural gas as the second source after coal, but that combined cycle power plants can play a crucial role as a flexible system support (AIE, 2009). Therefore, some studies (TREC, 2007a) deem it necessary to increase the gas storage capacity in the MPCs to stabilise the electricity grid given an increase in generation by renewable energies. The promoters of solar thermal energy note that this technology allows the incorporation of accumulation systems, as well as hybridising it with conventional fuels. In any case, the development of the gas market is one of the demands of countries such as Morocco and Tunisia in their European Neighbourhood Policy action plans.

Another of the constants of the studies consulted is integrating renewable energies in a desalination plan that explores the possibility of using renewable energy to feed water treatment plants. However, given that the UfM includes a programme of water treatment projects, this document will not develop its implications.[5]

Energy efficiency

Energy efficiency must become one of the strategic elements of the Mediterranean Solar Plan. It is also one of the objectives of the Community energy policy, which aims to improve it by 20% by 2020, and it is understandable that it tries to project these preferences towards its Mediterranean neighbourhood. From the perspective of the MPCs, supplying the aforementioned marked increase in demand means large investments, so that the application of efficient energy technologies is of the greatest importance. The degree of energy efficiency of a country is statistically calculated based on its energy intensity; in other words, the amount of energy necessary to generate a determined amount of GDP. It should be remembered that energy consumption per capita of some of these countries is very low, while their energy intensity is high, as shown in the following table.

Table 2: Energy consumption per capita and energy intensity: Low consumption and high intensity

| 2007 | Energy consumption per capita | Energy intensity | |

| Country/region | TPES/Pop. (toe/capita) | Electricity consumption (kWh/capita) | TPES/GDP (toe/000 2000US$) |

| World | 1.82 | 2752 | 0.30 |

| OECD | 4.64 | 8477 | 0.18 |

| Algeria | 1.09 | 903 | 0.50 |

| Egypt | 0.89 | 1468 | 0.49 |

| Spain | 3.21 | 6296 | 0.20 |

| France | 4.15 | 7573 | 0.18 |

| Greece | 2.88 | 5628 | 0.19 |

| Israel | 3.06 | 7010 | 0.14 |

| Italy | 3.00 | 5718 | 0.15 |

| Jordan | 1.26 | 1956 | 0.56 |

| Libya | 2.90 | 3880 | 0.36 |

| Morocco | 0.47 | 715 | 0.27 |

| Tunisia | 0.86 | 1246 | 0.33 |

| Turkey | 1.35 | 2210 | 0.27 |

Source: IEA, Key World Energy Statistics 2009, Paris.

In fact, the Middle East and North Africa region is among the most energy intensive of the world, just behind the former Soviet Union and Africa. Moreover, this data does not adequately reflect the traditional biomass consumption in some MPCs, which is why the real energy intensity is probably higher. This situation is partly due to differences in an intensive economic structure in the use of energy and in low GDP figures, but also to other elements, such as the use of obsolete technologies, the absence of incentives for efficient consumption and conversion, or the lack of resources and know-how in the maintenance and management of infrastructures.

Each of these elements offers several opportunities to improve the energy efficiency of the region, which would have significant economic implications. According to Ivanic and Martin (2008), the impact on GDP of improving energy efficiency between 10% and 50% in the countries considered in the table below would be, respectively, between $1,600 and $6,000 million. Blanc (2009) estimates that for Morocco, Egypt and Tunisia, a decline in energy intensity of 10% in 10 years would mean a decrease of 16% of consumption over the initial level; moreover, he notes that the highest potential is in the domestic sector, with an 11% decrease in consumption over the initial level, and only 5% in the industrial sector. The importance of the domestic sector not only has implications for the promotion of efficient standards in construction and electrical appliances, but at a broader level over better control of consumption through the introduction of meters, or even pre-paid meters.

Table 3: Impact on GDP of improvements in energy efficiency: A significant economic effect

| Country/Region | 10% | 20% | 30% | 40% | 50% |

| Egypt | 751 | 1,406 | 1,983 | 2,496 | 2,955 |

| Morocco | 189 | 353 | 497 | 624 | 737 |

| Tunisia | 125 | 233 | 328 | 413 | 488 |

| Rest of North Africa | 584 | 1,089 | 1,530 | 1,920 | 2,268 |

Note: in million $.

However, these calculations do not include electricity losses and, therefore, do not provide estimates about the impact of an improvement in the grid. Although to some extent the technical losses are inevitable, they can be significantly reduced with measures such as the improvement in the configuration and design of the grid, avoiding congestion and allocating more resources to maintenance. In this aspect, the potential of smart grids in the Mediterranean deserve to be explored in more detail, especially in terms of the potential power line grids. There is already experience of development cooperation in these issues. Specifically, the German cooperation agency (kFw) has several projects that deal with grid improvement, but also the generation installations and the installation of meters (Werner, 2007).

Although the measures to improve energy efficiency are highly diverse, they all happen because energy prices tend to reflect costs. Even technical aspects, such as losses experienced by the electricity grids of the MPCs, far greater than those of the industry standards, are related to the lack of incentives for the efficiency involved in the existence of generous energy subsidy schemes. Therefore, efficiency means a way of reducing the cost of subsidies, very onerous in some MPCs, without raising prices. In the context of low energy consumption of the MPCs, which in some cases such as remote rural areas result in energy poverty, the rise in energy prices has high social costs, has been strongly rejected and has resulted in numerous protest demonstrations by citizens.

The diagnosis of the energy efficiency situation in the MPCs, with obvious exceptions such as Israel, is not very encouraging. Although there have been advances in some countries, there is still much to do to bring together the basic prerequisites to permit the significant improvements in energy efficiency: commitments and clear policies in the long term; an adequate institutional, legal and regulatory framework; elimination of discretional subsidies; transparent conditions in the energy market; specific policies with financial and tax incentives, awareness-raising and training (RaL, 2007, p. 7).

The World Bank (2009) has a scheme for energy efficiency in the region based precisely on prices reflecting costs and the variations of supply in time. To deal with the social costs involved, it proposes a mechanism of subsidies focused on the lowest rent homes, given that current schemes tend to benefit those who need them least.[6] Although we will return to this subject as one of the difficulties posed to the regulation of renewable energies, among the MPCs we find diverse situations. With 2006 data, the impact of subsidies on energy varies between 1.3% of GDP for Morocco, 8% for Algeria, 12% for Egypt or 15% for Libya. In general, a first group of countries such as Morocco, Israel or the Palestinian Authority have prices close to costs; a second group of countries (Algeria, Jordan, Lebanon, Syria and Tunisia) have prices below costs, but not far off; and a third group of countries (Egypt and Libya) have prices far below costs.

The second stage of the strategy consists of developing a favourable institutional environment: legislation and regulation of energy efficiency, national strategies and specialised agencies. At present, several MPCs are beginning to have an institutional framework capable of managing the necessary reforms to improve energy efficiency and there are initiatives to this end, basically related to the creation or enhancement of specialised agencies and the regulation of codes of construction, standards, labels and energy audits (RaL, 2010). However, this institutional framework remains on occasions fragmented and is not always applied or its provisions minimally monitored. From this dual basis of prices, which reflect the real scarcity of energy and institutions that encourage efficiency, a third phase develops which involves carrying out sectorial programmes (for example, energy audits or rehabilitation of installations) and support programmes (such as social awareness raising, the development of ESCO agreements or agreements with academic and scientific institutions). Finally, funding programmes are also required, as access to it is one of the most common barriers to investments in energy efficiency, given the important level of the initial costs.

The Mediterranean Solar Plan could support some of these institutional actions and programmes through technical cooperation in institutional design, technology transfer and participation in specific training programmes. However, it must not be forgotten that any serious effort in terms of energy efficiency requires price adjustment.

The Need to Define a Credible, Predictable and Incentivising Regulatory Framework

Despite the advances made in recent years, as already mentioned renewable energies still require transitional stimuli that must be regulated.[7] They also need a stable institutional context that reduces the regulatory risk and allows us to undertake the major investments demanded by its high capital intensity, creating the appropriate conditions to establish a sustainable framework in the long term for their development. The legal security of investments in a region of high country-risk, as well as the stability of the incentives, are a necessary prerequisite before considering the payment schemes and the possibilities of funding of the different initiatives. Another important aspect is that of the technical standards, as the interoperability of the electricity systems demands their harmonisation. Although the standardisation of the technical requisites is being carried out gradually, the need to enhance technical cooperation to advance in this process should be emphasised.

| Box 3: Key principles for the design of a renewable energy policy The removal of non-economic barriers, such as administrative hurdles, obstacles to grid access, poor electricity market design, and lack of information and training.The need for a transparent and predictable support framework to attract investments.The introduction of transitional incentives, decreasing over time, to foster and monitor technological innovation and market competitiveness.The development and implementation of appropriate incentives guaranteeing a specific level of support to different technologies based on their degree of technology maturity to ensure technology diversification.The due consideration of the impact of large-scale penetration of renewable energy technologies on the overall energy system. Source: IEA (2008b) |

Box 3 summarises the five fundamental principles of the design of a policy on renewable energies according to the International Energy Agency. The analysis of the incentivising and legal measures adopted by the MPCs towards this design shows some progress, but at very different rates. We can distinguish between three groups of countries (Plan Bleu, 2008a and b). Morocco and Tunisia (to which Israel and Turkey could be added) would be the most advanced, while the hydrocarbon producing countries (Algeria, Egypt, Libya, Syria) would be those with the most renewable energy reforms pending. The rest of the MPCs would be placed in an intermediate position. However, all the studies agree on pointing out the existence of institutional and legal barriers, including the following (Plan Bleu, 2008; OME, 2008; Lafitte et al., 2009; Marín and Escribano, 2009; RaL, 2010):

- Absence or fragmentation of responsibilities in the area

- Lack of coordination of the bodies involved

- Non-existence or partial and/or longwinded application of the legislation

- Instability of the incentives

This situation demands the putting into practice of technical cooperation and training programmes to improve the legal framework and give greater analysis and monitoring capacities to the regulatory bodies and the authorities. Historically, the electricity markets of the MPCs have been state monopolies, but since the mid-1990s Morocco, Turkey, Tunisia and Egypt have begun to allow private participation in electricity generation. At present, around 16% of the capacity installed in these countries is in the hands of independent power producers (IPPs). Given that the monopolies persisted, power purchasing agreements (PPAs) were established with the IPPs, which were unable to attract the necessary investment. Consequently, some MPCs have started the liberalisation of their electricity market to offer more guarantees to investors, but the process is still insufficient, leaving a long and difficult road ahead that must be encouraged by the EU.

In addition to the questions related to the legal security of investments and access to the market, one of the essential elements of the regulatory framework is funding of renewable energies and the mechanisms used. Beginning with the tools, the modality with most consensus in the EU is that of the feed-in tariffs (FITs). However, there are other alternatives, such as tax incentives. For example, the USA applies a Production Tax Credits (PTCs) scheme,criticised for its lack of predictability in its renewal and the inability to indicate significant incentives in periods of low profits. Other schemes involve the use of quotas, tendering or investment subsidies.

The Third Legislative Package leaves its Member States free to adopt the payment model of its choice, basically FIT, tradable green certificates (quotas), tax incentives or tenders.[8] The FIT or bonus system seems to bring together most consensus and, in fact, is applied in most Member States.[9] It seems, therefore, to be the most appropriate scheme, although its effects depend on the existing administrative barriers and grid access (MEDREG, 2008). Some proposals indicate that, in the short term, Spain could extend its FIT system to electricity from renewable installations in Morocco (Ummel and Wheeler, 2008). On the other hand, the objective of developing 20 GW in 2020 seems difficult to achieve with the prevailing support systems and those in preparation in the MPCs, while the mechanisms based on FITs have shown their appeal in the EU and other emerging countries (RaL, 2010).

However, the problem is not so much the mechanism, but who finally pays the bonus, the MPCs themselves or the EU Member States (and which groups within them: consumers, tax payers, companies…), and the level of support provided. Given that the overall production cost of the electricity generated through renewable energies is currently, and with the aforementioned differences and qualifications, higher than that of conventional sources, their development represents an externality which is not taken into account by the market and requires State intervention. This intervention means a cost which must be directly or indirectly shared between States and, within them, between consumers, tax payers and companies. The first element, therefore, consists of ensuring a balanced, although not necessarily symmetrical, sharing of the costs between the EU and its member States and the MPCs. To a large extent, this will depend on the characteristics of the regulation of the electricity exports produced with renewable energies to the EU, but it does not seem efficient to move too far from the market logic. Thus, a generalised proposal lies in establishing a bonus slightly lower to that prevailing in the EU, or in the countries to which this electricity is destined, given that it is estimated that generation costs are lower in the southern Mediterranean (Lafitte et al., 2009; Marín and Escribano, 2009; RaL, 2010).

In terms of the support level, in the EU the lowest bonuses are applied to wind and hydroelectric energy, followed by solar thermal, while the bonuses for photovoltaic tend to be higher. In the southern arch of the Mediterranean, the bonus system is in force in Algeria, Egypt, Israel and Turkey, and under study in Morocco, Tunisia and Syria. Tunisia, Egypt and Syria offer subsidies for investment, and Morocco and Turkey are studying them. Morocco and Tunisia offer tax reductions (on VAT or tariffs). Some countries have national funds devoted to the development of renewable energies, such as the Fond National de Maîtrise de l’Energie in Tunisia or the Fond pour les Énergies Renouvelables included in the 2010 Algerian budget; moreover, the Moroccan solar mega-project (2,000 MW by 2020) has the support of the Hassan II Fund for Economic and Social Development.

Perhaps the most important obstacle is the high subsidy level which fossil fuels benefit from in most of the MPCs. In some countries, such as Morocco or Tunisia, these subsidies have tended to decrease slowly; but they continue to be considerable and undermine the competitiveness of renewable energies. Moreover, the variability of electricity consumption prices among MPCs is very high, ranging from the simple to the quintuple according to the country (Lafitte et al., 2009, p. 23; World Bank, 2009, p. 77 and ff.), but always below the generation cost of renewable energies (RaL, 2010, p. 53).

In the selection of incentive levels and mechanisms there is no approach to the Community acquis given that, despite the prevalence of the bonus system, Directive 2009/28 leave countries, Member States and third countries free to develop their own national support systems. Moreover, there are countries with a relatively easy access to the Community electricity market in the medium term, such as Morocco, and others, such as Egypt, more difficult to interconnect in the short and medium term. In the first case, the regulation must take into account both the support for exports of electricity generated with renewable energies and its national consumption, while, in the second, the regulatory problem is limited to the national market. Consequently, it seems that the only way to advance in the integration and regulatory convergence is the coexistence of regulatory frameworks. In strategic terms, the Mediterranean Solar Plan can mean the possible differentiation of the electricity corridors of renewable energies to adapt to the preferences of their possible partners.

In any case, the bonuses can be onerous for the MPCs. In Algeria, for instance, they represent up three times those of conventional energy tariffs. Thus, their generalised application to growing quantities of electricity generated with renewable energies can be limited, especially in the non-hydrocarbon producing countries, which have tighter budgets. Moreover, it seems that those MPCs which have managed to reduce at a significant political cost the subsidies for fossil energies and electricity (or even maintain them) cannot assume overly ambitious budget or tariff commitments in order to give priority to renewable energies.

Important Funding Costs and Needs Requiring Facilitating Mechanisms

As already mentioned, the materialisation of the Mediterranean Solar Plan requires the funding of some high costs. The cost estimates varies considerably according to the studies but, despite this dispersion, the amounts are in any case very high. The initial French-German posture on the Mediterranean Solar Plan of August 2008 anticipated the figure of €80,000 million, of which €10,000 million would be aimed at interconnections. For Lafitte et al. (2009) the estimated cost of the ‘solar +’ scenario is around €40,000 million, higher than the €32,000 million of the ‘wind +’ scenario due to the greater intensity of capital of solar energy, to which should be added €4,000 million to transmit 5 GW, plus an additional €2,000 million to connect the plants to the grid. ESTELA (2009) estimates a cost of €97,000 million until 2020 for 20 solar thermal GW, of which €16,000 million are for interconnections. The DESERTEC project estimates, for 10 GW in 2020, a cost of €42,000 million in investments in CSP plants and an additional €5,000 million for two HVDC lines (DLR, 2006).

They are high figures. The current list of projects has reached an investment of €25,000 million for around 10 GW (RaL, 2010). However, they do not include the costs related to risk coverage which, in any case, would accompany investments of these characteristics and which can mean considerable amounts, such as those related to the development of new technologies or the physical and legal insecurity. As previously mentioned, the REACCESS project of the 7th EU Framework Programme should soon provide more precise and adjusted estimates, specifying the optimum localisations and corridors from a broad perspective which takes into consideration technical, economic and geopolitical elements.[10] The challenge of mobilising the expected funding to reach 20 GW in 2020 requires important short-term incentives if the aim is to give credibility to the Mediterranean Solar Plan.

Moreover, these funding needs take place in a particularly difficult context. As a consequence of the shock of the international crisis, the size of the financial system has been reduced and there have been changes in its composition. Both elements have had an effect on energy businesses, which must operate under much more restrictive conditions. Although the interest rates have decreased and are still low, the cost of credit has fallen less, while obtaining funding has become much more complex for the energy sector.

The financial crisis has also seriously affected the real economy. The fall in growth has provoked a slump in the demand for energy, which has resulted, immediately and as per expectations, in a fall in energy prices. This decrease in demand and prices of traditional energies is discouraging investment in new energies, both in the research and extension and production phases. When there is a change in the conditions of the world economy it will be difficult to make investments in renewable energies and in transmission grids which have not been made during these years. The IEA (2009, p. 161) outlines that the fall of investments in renewable energies represents a major step back in the fight against climate change. Investments in these energies went from an increase of 85% in 2007 to a decrease from the last quarter of 2008 and fell by around 20% in 2009.

One of the objectives of the UfM lies precisely in facilitating the achievement of priority structuring projects such as the Mediterranean Solar Plan, mobilising the necessary funding. The financial markets in developing countries are characterised by a triple financial gap: insufficient funds, inappropriate terms and conditions, and lack of availability of financial instruments (KfW, 2005). This situation prevents them from mobilising the necessary financial resources for the mass development of renewable energies.

The question which has accompanied the whole of its constitutive process is about where these funds would come from, both at the level of the funding of investment or equity and tariffs. The Euro-Mediterranean Community funds have a clear budget allocation and are widely criticised for their limited level, in any case incapable of providing the funding necessary for the set of projects envisaged by the UfM, although the FEMIP (Facility for Euro-Mediterranean Investment and Partnership of the EIB) and the ENPI (European Neighbourhood and Partnership Instrument) could have a role. The approach for the funding of projects is based on the concurrence of public and private funds, Community funds, loans from the EIB and other international financial bodies, especially the World Bank, the African Development Bank and the regional Arab financial institutions.

Again, the projects incorporated into the Mediterranean Solar Plan may be the responsibility of different financial mechanisms. Thus, it is worth distinguishing between funds (funding or capital) for the installations of renewable electricity generation and transmission lines, on the one hand, and the training and technical cooperation programmes, on the other. The latter represent a category apart, whose funding could come from Euro-Mediterranean and bilateral cooperation. The funding of a supergrid could be the responsibility of a company with the participation of Transmission System Operators (TSOs), which in most of the MPCs and the Member States are public companies or regulated natural monopolies, and multilateral banks, especially the EIB. Another possibility is a broader consortium with the participation of distribution companies.

However, all the studies agree that mobilising the international financial institutions will not suffice to undertake such an ambitious plan. This requires a broad participation of private initiative and, specifically, of Foreign Direct Investment (FDI), largely affected by the international crisis in 2008 and 2009, as already mentioned. Initially there was consideration of the role of the sovereign wealth funds of the GCC countries, which could be interested in participating in a project such as the Mediterranean Solar Plan, in which they could participate first as financial backers and/or partners to later develop the technology in the Gulf itself. In fact, the participation of the Arab League in the UfM sought to bring together the Gulf countries to raise investment in the projects identified. However, these funds have been greatly affected by the financial crisis, to which we must add that the decrease in oil prices has reduced the contributions and increased the demands for domestic funding based on them.

The participation of FDI has the advantages of having no effect on public budgets, creating jobs, transferring technology, training human capital and developing new industrial branches. Although in the past the MPCs were not attractive for FDI, in recent years clear improvements have been made, especially in some countries. Consequently, one of the key issues for private initiative to find ways of funding is the context in which it develops its activity. The stability and clarity of the regulatory framework facilitates obtaining funding. Other regulatory aspects, such as the granting of a sufficient number of licenses to obtain economies of scale and advance in the learning curve also have an effect on the capacity to fund projects. In fact, OME estimates (2008) indicate that 70% of renewable electricity generation projects in the MPCs will be IPPs funded privately, a model related to free access to the market and regulation by bonuses. Foreign investment has shown interest in the potential of renewable energies in the southern Mediterranean. However, the public financial resources of the MPCs are not capable of supporting major incentives for renewable energies and, therefore, are not enough to generate an expansion in the market.

The limitations for the development of renewable energies in the southern Mediterranean markets therefore demand foreign funding of the installations and funding derived from a payment tariff framework for “renewable” electricity exported to the EU. Other measures could consist of acting on the tax pressure through tax abatements (VAT), agreeing subsidised loans and creating guarantee funds (or widening those already existing) that reduce the risk of the projects. The Private Public Partnership (PPP) seems to adapt well to projects involving major investment (solar power stations, wind parks) and has already been used by European companies in the region. Another possibility to reduce the risk of the projects is to enhance the role of energy services companies, providing them with participation in capital and guaranteeing the maintenance of the installations.

There has also been insistence on the need to generalise the use of the Clean Development Mechanism (CDM) of the Kyoto Protocol. The CDM is a financial tool which may encourage FDI in renewable energies in the MPCs, but which is being poorly used in the region. Among the projects submitted are wind parks in Egypt, Morocco and Israel, and the rural photovoltaic electrification programme in Morocco. The most common explanation is the lack of local powers to prepare projects, the lack of coordination between authorities and the almost non-existent involvement of banks and local companies. Moreover, investors must face the uncertainty over the price of emissions inherent in their volatility and the demands for additionality which may inhibit the application of the most innovative technologies. Other possible funding sources in the EU framework can be the GEREFF funds (Global Energy Efficiency and Renewable Energy Funds).

Finally, development cooperation can also contribute through the funding of installations that help fight energy poverty and improve income levels, as well as through technical cooperation and training programmes. Some countries have experience in the funding of renewable energy projects with development aid funds, for instance the Zafarana wind park in Egypt, which has benefited from loans and donations from the KfW and Danish and Spanish development agencies. Although some analyses estimate that the support of donors must concentrate on the technologies closest to the profitability threshold (KfW, 2005), we must not ignore the potential of the MPCs to descend the learning curve. Thus, technological cooperation for sustainable development is another of the development cooperation lines which could be best developed by the EU.

All these options to support the development of projects related to the Mediterranean Solar Plan have been summarised as follows (RaL, 2010, p. 73):

In recent years, interesting initiatives have been launched. In the UfM ministerial meeting on sustainable development held in Paris, the EIB, the German Development Bank (KfW) and the French Development Agency (AFD) announced a joint investment programme of €5,000 million for renewable energies. In April 2009 in Alexandria, InfraMed was launched, a long-term investment fund which will complement the FEMIP by investing, among other projects, in energy infrastructures. The instruments can include donations and subsidised loans.

One of the most important projects is the Clean Technology Fund Investment Plan for the development of the CSP launched by the World Bank in late 2009. This plan seeks to accelerate its development in Algeria, Egypt, Jordan, Morocco and Tunisia, until reaching 1 GW, as well as to support the related transmission infrastructures. The Fund proposes the co-funding of $750 million and the mobilisation of an additional almost $5,000 million.

The Mediterranean Solar Plan as a Euro-Mediterranean Vector of Integration

One of the declared objectives of the UfM is to carry out structuring projects to complement the processes of commercial and regulatory integration initiated by the Euro-Mediterranean Partnership and the European Neighbourhood Policy, respectively. The Mediterranean Solar Plan constitutes a vector of regional integration, not only between the EU and the MPCs but also between the Member States themselves and the MPCs (Marín and Escribano, 2009). In the previous section we outlined the reduced current degree of electricity interconnection between the shores of the Mediterranean and the need to strengthen it, as well as the additional effort of interconnecting the MPCs, so as to transmit the electricity generated with renewable energies. The variable nature itself of renewable energies requires greater flexibility of the electricity grids in order to increasingly integrate them into the energy system (IEA, 2008c).

The emphasis on regional integration in functional aspects such as those related to energy is a constant in Euro-Mediterranean relations. The Ministerial Declaration of the Euro-Mediterranean Energy Forum held in Athens in 2003 considers the integration and full interconnection of the regional energy market to be one of the key objectives of the Euro-Mediterranean energy partnership, along with the objectives specific to the Community energy policy (security, competitiveness and sustainability) and the promotion of renewable energies. To this end, the Forum pointed out the need to harmonise rules, standards and statistics and to facilitate the funding of energy infrastructures in the region. The Euro-Mediterranean Energy Forum, held in Brussels in 2006, insisted on the need to undertake a process of regulatory convergence to achieve the objective of a fully integrated Euro-Mediterranean energy market, and noted the possibility of enlarging the Energy Community Treaty to the MPCs.[11]

The 2005 Barcelona Euro-Mediterranean Summit adopted a 2005-2010 programme, which included among its objectives the electricity integration of the Mashreq and the Maghreb with the European network. The Limassol Ministerial Conference (2007) adopted a Priority Action Plan 2008-2013 with three objectives: to support the reforms of the MPCs, gradual harmonisation, and integration and interconnection of markets. One of the measures envisaged to advance in the regulatory harmonisation was the consolidation and expansion of the MEDREG activity. In 2008, the second Strategic Energy Review (SER), along with a commitment to the networks, emphasised among its international cooperation priorities the completion of the Mediterranean Energy Ring in order to improve energy security and help develop the potential of renewable energy resources in the region. This aspect will be the object of a Communication of the Commission in 2010.

Despite these efforts, the interconnection of the European markets and those from southern and eastern Mediterranean countries is limited. In this context, in order to play a role as an element of regional structuring, the Mediterranean Solar Plan must confront at least three main challenges: the creation and/or strengthening of the necessary interconnections and electricity grids, the design of a regulatory mechanism encouraging a real integration of the sector, and an institutional framework allowing the regulatory convergence between the countries involved.

Addressing the physical integration through the creation of electricity interconnections and the necessary grid improvements

The establishment and development of the trans-European energy grids is one of the main objectives of the Community energy policy and is envisaged in the Lisbon Treaty, which also stipulates that the Community will act to promote the interconnection and interoperability of the national grids. The Treaty permits cooperation with third countries to promote projects of joint interest and to ensure the interoperability, especially through technical standardisation. It also introduces the concept of solidarity in the field of energy, which in its turn requires, among other elements, the existence of cross-border interconnections so that it can be applied. The debate on the new Energy Security and Infrastructure Instrument can also be applied to the interconnections necessary for the operation of the Mediterranean Solar Plan.

In the context of the trans-European energy grids some guidelines have been developed to promote projects based on their categorisation in projects of joint interest, within which those with a relevant impact in terms of environment, security, supply and territorial cohesion are considered a priority. The cross-border priority projects or those with relevant impact on the cross-border transmission capacities are considered of European interest and have priority in the budget of the TEN-E project and other Community budgetary items. The third countries involved in the projects must facilitate them in their territory in keeping with the Energy Charter Treaty.[12]

The studies carried out tend to outline the advantages of the HVDC lines because of their lower losses in long distances, especially in terms of underwater cables (PWC, 2010; MED-EMIP, 2010). The HVDC power lines for transmission of the electricity generated with renewable energies in the MPCs could mean, in fact, the interconnection of the European electricity markets and would be in keeping with the objective of a single electricity market. This aspect is of special importance for the Mediterranean Partner Countries, which suffer a relatively important isolation from the European energy market. Without the development of interconnection infrastructures between Mediterranean Europe and the rest of the European continent, electricity is unlikely to be transmitted from the MPCs to the EU. To be specific, it is essential to enlarge the clearly insufficient and saturated electricity interconnection between France and Spain to advance in Euro-Mediterranean electricity integration (RaL, 2007). Table 4 provides four energy imports profiles. Profile 4, which could be called the Mediterranean profile, shows a reduced integration in the European energy market and a clear projection towards the southern Mediterranean.

The North Africa-southern Europe interconnection would blur the differences between profiles 1, 2 and 4 and bring Mediterranean Europe closer to a more European profile, given that profiles 1 and 2 would possibly see their energy imports (in this case electricity) from the Mediterranean region increased. Thus, the France-Spain interconnection would mean the Europeanization of the Mediterranean Member States, but also the “Mediterraneanization” of the non-Mediterranean Member States. Moreover, the development of the electricity interconnections would allow the application of the principle of solidarity, currently limited by the impossibility of transmitting electricity or gas from determined Mediterranean markets to the rest of the EU. In many aspects, the development of the trans-European gas and electricity grids cannot be dissociated from the development of renewable energies in the MPCs and the export of electricity to the EU. Finally, EU security would increase while its vulnerability would decrease, in keeping with the objectives of the Community energy policy.

Table 4: Characterisation of the EU Member States according to origin of their energy imports: Four highly differentiated Europes

| PROFILE 1: Predominance of intra-European imports (76% on average) and moderate weight of Russia and Central Asia (11% on average) and North Africa (5% on average) | ||

| Austria | Ireland | Slovenia |

| Belgium | Luxemburg | Sweden |

| Denmark | Malta | UK |

| PROFILE 2: Predominance of intra-European imports (44% on average) but high imports from Russia and Central Asia (41% on average) and moderate contribution of the Middle East (6%) and North Africa (5%) | ||

| Czech Republic | France | Latvia |

| Estonia | Germany | Holland |

| PROFILE 3: Clear Russian predominance (81% on average together with Central Asia) and moderate intra-European weight (17%) without significant participation from other origins | ||

| Bulgaria | Hungary | Poland |

| Finland | Lithuania | Rumania |

| Slovakia | ||

| PROFILE 4: Reduced participation of intra-European imports (22% on average) with elevated weight of the Middle East (27%), North Africa (17%) and sub-Saharan Africa (8%) | ||

| Cyprus | Italy | Spain |

| Greece | Portugal |

Source: REACCESS-UNED (2009), table 9, p. 21.

Note: calculated with aggregated data for 2006

In the southern Mediterranean, the completion of the Electricity Ring goes beyond the economic field to take on political connotations (Renner, 2009). In this aspect, we should point out that the Maghrebian electricity interconnections do not take place in a particularly favourable political context. The promotion of the electricity ring has therefore become a medium and long-term imperative for the development of the Mediterranean Solar Plan, as a regional and large scale development of renewable energies for exporting electricity to Europe requires enhancement of the interconnections between the MPCs themselves. And the Ring, in its turn, involves the type of structuring integration consistent with the UfM. Among the conclusions of the MED-EMIP study (2010) on the Mediterranean Ring, three options are put forward to allow the exchange of large amounts of electricity between the two shores of the Mediterranean: the enhancement of the existing connections in the Strait of Gibraltar and the Bosporus, underwater corridors with HVDC lines or a combination of the two.

Finally, the existence of electricity corridors is one of the determinants of the localisation of the generation capacities of green energy, the type of technologies applied, the power installed and the future marginal generation cost (Vajjhala et al. 2008). For instance, the investment plan of the Clean Technology Fund for the CSP in the Middle East and North Africa includes two interconnection projects, one in Jordan to strengthen the connection with Europe and another between Tunisia and Italy, which would have important implications from the perspective of localisation of CSP installations. Something similar happens with the proposal made by MED-EMIP (2010) shown in Map 3 and already commented. The generation installations are constructed where there is grid access, which in its turn determines the optimum type of generation technology and capacity and, therefore, the cost. Moreover, this means that the layout of the corridors of electricity generated from renewable energies must be coordinated with the policy of support for renewable energies to guarantee the consistency of the measures.

Designing credible regulatory mechanisms encouraging a real integration of renewable energies into the Euro-Mediterranean area

Although the Community acquis includes numerous provisions on trans-European energy grids and the participation of third countries in joint projects of European interest, the new Directive 2009/28 on renewable energies regulates the mechanisms under which these joint projects can be undertaken. The Directive notes that the State Members only support the renewable energy generated in their territory and points out that one of its aims is, in fact, to facilitate cross-border support for renewable energies without affecting the national support systems. To this end, it introduces cooperation mechanisms between Member States allowing them (1) to agree on the degree of support granted by a Member State to the renewable energies of another; and (2) how to share the production with a view to the national objectives established by the Directive itself. The measures of flexibility between Member States include statistical transfer, joint projects and, also, joint support systems.

For the electricity generated with renewable energies imported from third countries, the conditions are less flexible, given that statistical transfer is not permitted. Although the physical imports from third countries can be included within the objectives of the contribution of the renewable energies by the Member States, in order to ensure the additionality[13] only those based on new installations or capacity enlargements existing ones which enter into operation following the implementation of the Directive will be taken into account. To this end, the Member States can undertake joint projects with third countries, and can include in their national objectives (1) the imported electricity generated with renewable energies consumed in the Community; or (2) the amount agreed in the joint project of the electricity generated with renewable energies in the third country until the interconnections are available.[14]

Given that the Directive does not affect the national support systems, there should be no obstacle to implementing joint support systems for these joint projects with third countries. The only limitation established is that, logically, to be included in the national objectives, the electricity imported cannot have received any help from a support system of a third country, with the exception of the aid for investment in the installations. Although statistical transfer to third countries is excluded, the Directive itself points out that the measures of flexibility for Member States could also be applied to the contracting parties of the Energy Community Treaty, if so decided.

In short, the new Directive stipulates conditions generally favouring the submission of joint projects between Member States and the MPCs and does not impede the implementation of joint support systems. Given that the Commission itself has stated its preference for the FIT/bonus mechanism prevailing in Germany and Spain, it seems that an adequate scheme could consist of enlarging this support system to the green imports from the MPCs. The FIT mechanism itself, linked to production costs, allows differentiation of the bonus granted to the electricity generated with renewable energies in the territory of the Member State and that received by a third country, which has lower costs, for instance due to more favourable climate conditions. With a view to 2020, it would be important to advance in the specification of feasible short-term projects and schemes, scalable at a regional level, allowing comparison of different integration models and providing greater credibility to the Mediterranean Solar Plan.

Establishing an institutional framework facilitating regulatory convergence between the participating countries

The third element necessary for the Mediterranean Solar Plan to become a vector of regional integration is the regulatory convergence required for the joint support projects and schemes to be operative. The interoperability of the electricity systems, the control of the support mechanisms, the transparency in public bidding conditions, authorisations, certifications and grid access, among other elements, require a minimum harmonisation, both technical and regulatory. The problem of regulatory convergence is inseparable from the very nature of the EU and its relations with the European neighbourhood and has been well studied by the European literature. The EU itself has been defined as a “regulatory power” (Manners, 2002), which resorts to the transformative power of the Community acquis (Magen, 2007) as an element of exterior governance (Lavenex, 2004).[15] In the Mediterranean energy area, this implies converging towards a model (Barbé et al., 2009) and accepting that this model can mean convergence in the objectives, but not necessarily in every one of the instruments (Bicchi, 2006).

This European approach to regulatory convergence in energy terms appears at several levels. The Directive on Renewable Energies itself is a pertinent text for the European Economic Space. The Energy Community Treaty is, in fact, based on enlarging the Community energy acquis and has been characterised as an energy enlargement (Simurdic, 2009). Other Community initiatives, such as the Neighbourhood Policy Action Plans and, to a lesser extent, the Euro-Mediterranean Partnership, contain elements of selective convergence in terms of energy. The recent EU-Morocco Advanced Statute also includes regulatory and technical harmonisation contents which enhance those of its Neighbourhood Action Plan.

One of the possibilities for providing a framework of comprehensive integration based on convergence is to extend the Energy Community Treaty to the MPCs. This would involve shaping the energy systems of the MPCs in the image of the Community acquis. However, the regulatory convergence allowing integration of renewable energies into the Euro-Mediterranean space does not necessarily require the integral and rigid application of all the Community acquis. Moreover, this maximalist approach does not currently seem feasible, given that the Treaty contains provisions in terms of grid energies, gas and electricity, very difficult for most of the MPCs to take on. By way of example, we can mention the posture of Algeria in favour of a differentiated agreement with the EU as an alternative to a Neighbourhood Action Plan (Darbouche, 2009). In contrast, the different preferences of the MPCs in several energy fields must be taken into account differently for each energy corridor (Escribano, 2010).

Thus, rather than a single integration model, it seems that there is a need for a differentiated variable geometry system for the electricity corridors based on renewable energies originated in the MPCs. The mechanisms of joint support projects and systems provided by Directive 2009/28 allow the establishment of regulatory frameworks specific to the context for the integration of the electricity generated with renewable energies in the MPCs in the electricity market of the EU and the MPCs themselves. These mechanisms can take place first in the framework of bilateral cooperation to later extend to the sub-regional level and, possibly, to the regional level. This approach also allows a softer transition towards more rigid integration schemes, such as that provided by the Energy Community Treaty. Moreover, the specification of simple and flexible integration schemes would improve the visibility of the Mediterranean Solar Plan and its credibility.

Directive 2009/28 limits the possibility of including the objectives of renewable energies established for the physical imports of third countries and maintains a certain imprecision in terms of the capacity to undertake joint support schemes with them. In contrast, it envisages the possibility of granting the members of the Energy Community a treatment identical to that of the Member States. Thus, it could be deduced that extension of the Energy Community Treaty to the MPCs would make it possible to also include the statistical transfers and, of course, to design joint support schemes. However, as already mentioned, the full extension of the Treaty to the MPCs does not seem feasible in the short term, given the commitments it involves in terms of electricity and natural gas. Moreover, although some countries, such as Turkey, or possibly Morocco, are relatively prepared for it, such differentiation could mean a greater fragmentation of the Mediterranean energy space. Thus, an initiative inspired by the Energy Community Treaty, although at first limited to renewable energies, could mean an alternative in the short term.

Renewable Energies as a Vector of Sustainable Economic Development in the Mediterranean