From one crisis to another: initially only slightly affected, the Southern and Eastern Mediterranean Countries eventually felt the impact of the second round of the global economic crisis that particularly struck the Euro-zone countries, the main trade partners and premiere investors in the Mediterranean Region. The repercussions of the Arab Spring significantly influenced the evolution of foreign direct investment (FDI) in the region in 2011 and 2012.

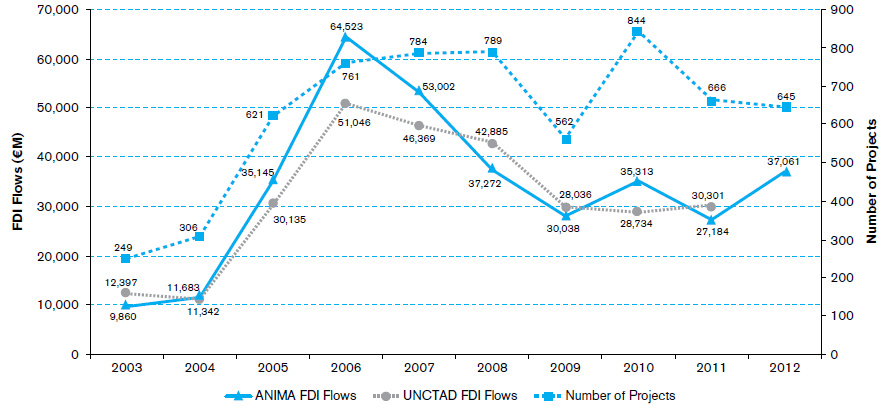

According to the United Nations Conference on Trade and Development (UNCTAD), FDI flows to the Southern and Eastern Mediterranean Countries, or the Med-11 (Algeria, Egypt, Israel, Jordan, Lebanon, Libya, Morocco, Palestine, Syria, Tunisia and Turkey) experienced remarkable progress up until 2006 (Chart 1), an exceptional year during which the countries in the region finally attracted a share of world FDI equivalent to their demographic weight (approximately 4%). This peak was reached thanks to a series of mega-projects in the banking, telecom, energy, and construction and public works sectors, essentially initiated by Gulf State investors. Foreign investment in the Med-11 thereafter entered a phase of decline, with a record drop in 2009, as per the global trend in FDI flows.

Since then, recovery is lagging. According to the ANIMA-MIPO observatory, which gathers information on FDI project announcements,[1] the strong revival of foreign investor interest in 2010 was completely cut short the following year by the onset of the Arab Spring. The political transitions shaking the vast majority of Arab Mediterranean countries have, in fact, caused an immediate drop in FDI project announcements: 666 projects were announced in 2011 amounting to 27 billion euros, the lowest level since 2004. Though the number of projects did not rise in 2012, the total amount of FDI funds (37 billion euros) was comparable to that of 2005 (before the peak in 2006) and 2010 (after the financial crisis and before the Arab Spring). In any case, this regional evolution conceals contrasting national situations, significant changes in investment origin and an encouraging trend towards sectoral diversification of FDI projects in the region.

CHART 1 Evolution of Investment Amounts and Number of FDI Projects Announced (in millions of euros)

Foreign Investment during the Arab Transitions: Relatively Good Resilience

Foreign investors are far from deserting the region despite the political uncertainty prevailing in many countries, the supply and security problems, and social movements that could have affected the operation of enterprises in 2011 and again in 2012. Hence, in amount of FDI announced, 2012 was the 4th best year of the past decade: with the exception of Syria, all countries registered FDI amounts in keeping with their average performance over the past few years (Chart 2).

CHART 2 Monetary Amounts of FDI Projects Announced by Country (in millions of euros)

In the Maghreb, first of all, Algeria experienced a good year in 2012, after two unproductive years: foreign investors seem finally to have adapted to the Law 49-51, which requires them to become associated with local enterprise. Morocco, often considered a country that was spared the unrest shaking the region, likewise experienced an encouraging rise in amounts invested. In Tunisia, the results were commendable, considering the political transition still underway in 2012, essentially thanks to extensions of projects announced by foreign corporations already operating in the country. The political and economic reforms of the coming months will be crucial for continuing to reassure investors and attract them to the “new” Tunisia. And in Libya, investors returned, with a record of 26 partnership projects[2] announced in 2012, paving the way for future investment projects.

In the Mashreq, the situation was more complex. In Egypt, the number of FDI projects announced did not really rise in comparison to 2011 due to the uncertain political and security situation. In any case, the country did register a record number of partnerships, and the amounts of FDI announced were on the rise again thanks to 3 mega-announcements of over a billion euros in the telecom and banking sectors. The foreign investment situation did not change significantly in 2012 in Lebanon or Jordan: FDI announcements were consistent with their historical levels, despite the proximity of these two countries to the conflicts shaking the region and the sensitive domestic political contexts. Palestine attracted 3 FDI projects (launched by the American Google company and the French communications group, Publicis), as well as 2 partnerships, making 2012 a relatively good year. Finally, no projects were officially announced for Syria in 2012.

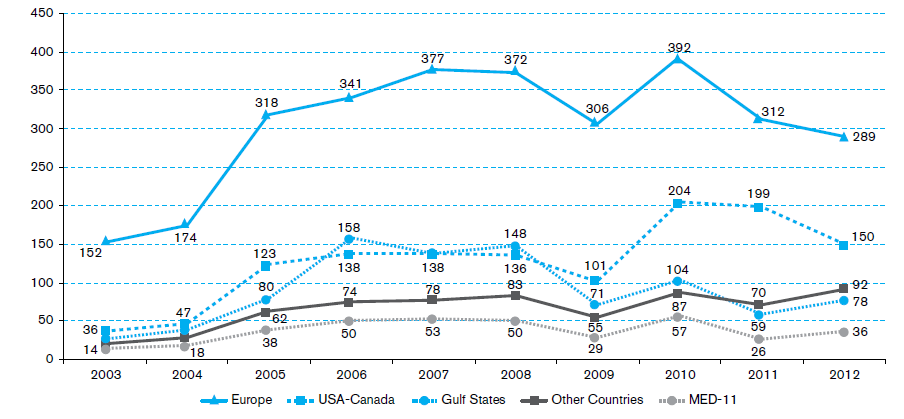

European companies have been responsible for half of the FDI announcements in the Mediterranean Region since 2003. This was still the case in 2012, but two factors indicate that this leadership is now seriously threatened

And finally, Turkey emerged as an increasingly undisputed regional leader, insofar as recipient country of FDI flows but also as an intra-regional investor: no less than 10 Turkish projects were announced in Mediterranean countries in 2012, 3 of them in Israel, 2 in Egypt, 2 in Algeria and 2 in Morocco.

Erosion of European Leadership and Rise of Emerging Countries

European companies have been responsible for half of the FDI announcements in the Mediterranean Region since the creation of the ANIMA-MIPO observatory in 2003. This was still the case in 2012, but two factors indicate that this leadership is now seriously threatened: the number of European FDI projects announced was at its lowest level since 2005 (Chart 3), and the investment sums announced by Europe were surpassed by that of “other countries” for the first time, in particular the BRIC countries (9.8 and 10.8 billion euros in 2012, respectively; see Chart 4).

This downtrend is most likely cyclical, European companies probably being influenced by the “anxiety attacks” and inaction that has seized European governments and their administrations vis-à-vis the new political leaders in the South Mediterranean. Yet in this period, when the Mediterranean Partner Countries (MPCs) are revising their development and governance models, basing them on new, democratic values, such diffidence on the part of Europe is both a bad strategic calculation and a poor interpretation of the Southern countries’ expectations of their historical partner.

At the same time, the Gulf States seemed to demonstrate a will to step up economic and political ties with Islamist governments having recently come into power in Northern Africa. After having abandoned the terrain from 2007 to 2011, their investments in 2012 were at the same level as those from Europe, reaching levels more in line with what Mediterranean countries could expect of their Arab neighbours. This vintage year of 2012 also probably marked the end of the financial crisis for the Gulf monarchies.

CHART 3 Origin of Announced FDI Projects (number of projects)

CHART 4 Origin of Announced FDI Amounts (in millions of euros)

The Western slowdown also applies to North America: whereas the projects announced by American and Canadian investors had not diminished in 2011, including in Arab countries – illustrating the North American will to acknowledge the revolutions underway – 2012 marked a return to greater restraint. The number of projects announced by the United States decreased in all the countries in the region, particularly in the Mashreq (only 3 projects announced for Egypt as compared to 13 in 2011, for instance), except for Palestine, and in Tunisia (3 announcements, as compared to 9 in 2011).

Intra-Med-11 investments also remained very low (6% of the total). One can, however, express the hope that the changes taking place will lead to greater political and economic integration in the region. There were some encouraging signs in this respect in the Maghreb, essentially thanks to the impetus supplied by Tunisia.

Towards More Inclusive FDI Projects? The Paths of Renewed Partnership with the Mediterranean

Fortunately, the crises seem to have had the consequence of fostering a certain sector rotation of foreign investment projects in 2011 and 2012. The traditional foursome of energy, banking, telecom and construction and public works continued to attract a record share of FDI (65% of the amounts announced in 2012), while a number of industrial sectors gained in attractiveness and became less marginal with respect to “rentier” investments – excellent news for Mediterranean countries. The number of announced FDI projects in software, the automotive sector and pharmaceuticals thus experienced a slow but steady progression, whereas aeronautics and the engineering industry registered a sharp rise in 2012. The agribusiness and food processing, distribution and business services sectors, which had attracted a record number of projects in 2011, on the other hand, were less popular with investors in 2012, due to the decline in European and American FDI.

The sectors experiencing growth are doubly strategic for the region: they contribute to structuring the industrial fabric of Med-11 countries and are, above all, more effective in terms of job creation. Indeed, the job efficiency ratio of foreign investment projects, developed by ANIMA through the ANIMA-MIPO observatory for the World Bank in 2011,[3] reveals that foreign investment in the Mediterranean Region is concentrated in sectors tending to create relatively little employment (with the exception of the banking sector). This situation constitutes one of the factors accounting for the currently low spillover effect of foreign investment on growth and inclusive development of the Med-11.

It is the arduous task of the southern countries to address the challenges associated with both their political transition and the establishment of a more transparent economic governance, in order to bring Europe back into a dialogue that is currently inoperative and develop a policy adapted to their needs

More than ever, the number one challenge in the region is, in fact, that of job creation. This is true in the South Mediterranean, where the problem of unemployment and particularly lack of quality jobs is a core concern of the population having demanded the political transition. It is likewise true in Europe, where growth is struggling to restart and struggling even harder to create employment.

In the face of this challenge, Europe can no longer ignore the issues blocking the economic vitality of the entire Euro-Mediterranean Region, i.e. the mobility of goods and people that are today’s and tomorrow’s economy, the education of people in the South, recognition and promotion of Euro-Mediterranean sectoral value chains, shared values and the sustainability and inclusiveness of domestic and foreign investment.

It is on the basis of developing an industrial area on the Euro-Mediterranean scale that a renewed, balanced and politically-focused partnership should be established between Europe and the South Mediterranean. It is the arduous task of the Southern countries to address the challenges associated with both their political transition and the establishment of a more transparent economic governance, to clearly establish their economic, industrial and social development strategies in order to bring Europe back into a dialogue that is currently inoperative and develop a policy adapted to their needs.

Notes

[1] In other words, projects announced by an investor in year n, which are generally carried out that year or in the following ones. The ANIMA-MIPO data thus differ from those of UNCTAD, which reflect real investment flows after the fact. The former are anticipatory data that have the advantage of being available in real time and provide information on the origin of projects (nationality of the investor, company type), the sectors concerned, etc. For more information, see www.anima.coop/mipo

[2] Understood as projects where a foreign company approaches a Mediterranean market either through an identified partner or by opening a local branch (these projects are equivalent to UNCTAD’s “non-equity modes of entry”).

[3] ANIMA. Mediterranean niches & sectors with high potential of job creation & growth. Background report for the CMI Draft Report on Transforming Arab Economies: The Arab and Knowledge Road, CMI, World Bank. 2011