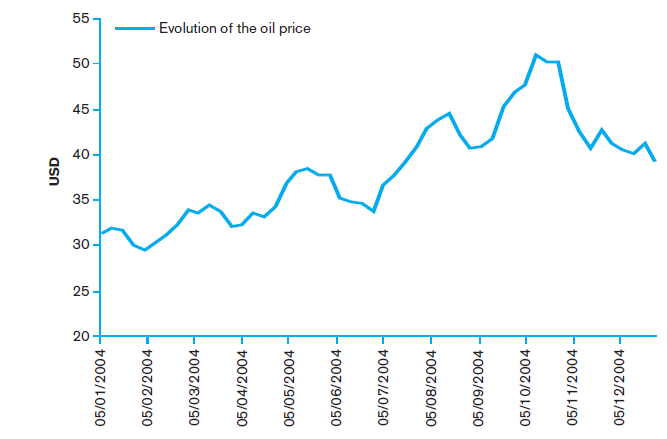

The year 2004 was marked by a major increase in crude oil prices: in December 2003 the international price of a barrel stood at USD 29.29, while by November 2004 it had already reached USD 44.49/barrel[1]. Although in real terms this price is still significantly below the levels of the 1980s, it is nonetheless a fact that in the first eleven months of 2004 the price of crude rose by 52.2%, thus breaking the psychological 40 dollar barrier. It is generally believed, that in such a situation -of significant increases in the price of crude over a short period of time-, the producing countries make a profit, as by selling the same quantity of oil they see their export income rise considerably, while the consumer countries lose, because for them this increase represents a greater expense in terms of imported energy supplies. This raises the cost of energy and hence it affects inflation rates negatively. Such a concept could thus lead us to the conclusion that within the Euro-Mediterranean area, which includes both types of country, an increase in oil prices would have an asymmetric impact: on the one hand, the (producing) countries of the southern coast, such as Algeria, Libya, Syria and Tunisia would gain, while the European (consumer) countries would be the losers. However, this image of the Mediterranean oil trade as a game in which the countries involved are either winners or losers, fails to reflect the true complexity. To begin with the producing countries, an analysis of the net export income of the two main oil-producing countries in the region, Algeria and Libya, indicates that as a result of the increase in oil prices, Algeria, in 2004, gained USD 22.6 million, and Libya 18.1. However, behind these figures exists a reality which indicates that as the energy sectors in these countries are gradually opened up and deregulated, we should also begin to consider the gains and losses of the companies operating within Algeria and Libya. Taking Algeria as an example (of the two, it has opened up its fossil fuel sector more extensively to foreign investment) we see that between the end of 2003 and the end of 2004, over fifty foreign companies were operating within Algerian territory. The result of this is that part of the oil which comes out of Algeria is not Algerian any more and that therefore a proportion of the income obtained through its sale on the international market is not either.

GRAPH 1 Evolution of the oil price (2004)

This can be seen from just three figures. According to the first, based on data from the Algerian Energy and Mines Ministry, at the end of 2003, 40% of crude and condensed oil produced in Algeria did not belong to the Algerian national hydrocarbons company, SONATRACH[2]. The second figure indicates that at the end of September 2004, almost 16% of income from crude and condensed oil exports belonged to foreign shareholders in SONATRACH[3]. Thirdly and finally, we can see that although the energy companies operating in Algeria have seen their profits rise with the increase in prices, this is true to a much lesser extent for the Algerians, since, proportionally, the figures show that the taxation take from these companies has fallen by approximately 40% since 1993[4]. In other words, the proportion of income which can be redistributed to the country’s population is in fact falling. Nonetheless, the case of Algeria does show that such significant increases in prices, as those we have seen over the past year do yield profits for those countries where hydrocarbon oilfields are to be found; but these profits are shared out among foreign companies, the national company (in this case SONATRACH) and the Treasury, in proportions which depend on the limits established for foreign holdings and the hydrocarbon taxes applied by each nation’s oil industry legislation. Recent years have seen changes in the international energy scene (IES). On a global scale, legislation has sought to privatise and transnationalise energy companies. This has given private companies on the IES a greater influence, to the detriment of producing states (and their national companies) and of the governments of consumer countries. The corollary of this is that the more open, deregulated and liberalised the energy sector is in producing countries, the lesser the effect of changes in the price of crude on the national income of these. Indeed, over the last year, if the figures are to be believed, Algeria has profited less than Libya in terms of national revenue. If we extrapolate from this situation to consider the other more minor producers in the region (Tunisia, Syria and Egypt), we may affirm that their gains or losses as a result of major variations in hydrocarbon prices, in terms of the national economy, will also depend on the degree of openness and deregulation within their energy sectors. We would therefore suggest that the more the process of signing Euro-Mediterranean Association Agreements continues -which is also connected with the openness and deregulation of the oil industry-[5] the less significant the effect of an oil boom on the national economies of the Mediterranean regions rich in hydrocarbons. Determining the effects of the recent oil boom on consumer countries in the region is a more complex task, although the data available for last year indicate that the presumed negative effect was not as great as had been expected, bearing in mind the experience of the Seventies and Eighties. In 2004 the economy of the Eurozone countries seems to have been affected more by the sharp rise of the euro against the dollar than by the increase in the price of crude. Thanks to this rise in those Eurozone countries, the price per barrel rose from EUR 25.10 in 2003 to EUR 30.50 in 2004[6], an increase in the price of crude within the Eurozone of 21.5%: significant, but much less so than the increase of 52.2% in dollar terms. This first issue could be seen as a factor of the economic cycle, but there is a second aspect which seems to be structural, and which could suggest that today an economy such as that of Europe is less vulnerable than in the past to sharp rises in the price of crude. In 2004, the increase in the price of crude does not seem to have had a major impact on the general level of prices, although there are clearly differences between countries. On average, across the Eurozone the Harmonised Index of Consumer Prices (HICP) varied between 2.2% and 2.4% for this period.[7]. Such a rate of inflation is not substantially different from that for the previous two years and so cannot be attributed to rising crude prices. The only slight effect of rising crude prices on the general level of prices indicates that, since the Eighties, the situation of the consumer countries has changed considerably. In the first place, because the diversification in the energy sector which has occurred since that time means that currently only 38% of primary energy consumed in the European Union comes from oil. In second place, because energy-saving policies have substantially reduced the quantity of energy used per production unit, although the transport industry continues to be the major consumer. Since 1990, energy used in the European industrial sector has fallen by 23.8% and that of the tertiary sector by 22.6%, while the figure for the transport sector is a mere 3% lower.[8]. Despite this, among Europe’s economies as a whole over this period, energy intensity has fallen in real terms from 245.6 (toe of energy consumed/M Euros of GDP) to 208.8[9]. We should therefore be talking of a reduced importance of oil for European economies and a reduced importance of energy costs for the majority of economic activity in the EU.

The obvious consequence of all this is that the losses which European countries were expected to suffer as a result of the sharp rise in oil prices have been far lower than had been predicted.

In summary, the information provided by the oil boom in 2004 is as follows. In the first place, it seems quite clear that if the countries of the southern shore of the Mediterranean continue to internationalise their energy reserves using the same criteria as they have this far, the future effects of changes in the price of crude will be minimal on the -national- economies of North Africa and the Middle East. And secondly, it does not seem that the economies of Europe are especially vulnerable to these price fluctuations, as they depend to a lesser degree than in the past on energy from oil. Despite this, the future effects of an increase in crude oil prices on these economies are unclear, because thanks to the increasing deregulation applied to the energy sector, companies within this sector have the power -the market- to alter these prices in accordance with business strategies which may have little or nothing to do with the needs of consumers. The surge in prices over the last year has therefore taught us that it is increasingly difficult to talk of an asymmetric impact with differing effects on producing and consumer countries. Indeed, given the changes which took place in the IES during the final decades of the 20th century and the growing internationalisation and transnationalisation of national energy sectors, the term producing country ceases to have any real meaning. The corollary of this is that an increase in oil prices leads to an increase in the profit margin for businesses, to the detriment of the income of producing countries (export national revenue). It remains to be seen what will happen with the income of consumer countries.

Notes

[1] Source: EIA (2005);OPEC revenues. Country details.

[2] Source: MEM Algérie (2005); Realization of Production: Hydrocarbons, Electricity, Petrochemistry

[3] Source: MEM Algérie (2005); Evolution hydrocarbons exportations

[4] Source IMF (various years); Algeria: Statistical Appendix and own calculation. This calculation is based on the relative taxation take for the hydrocarbons sector. In other words, the percentage tax take from the oil industry within government revenue as a whole/the weight of the sector within the GDP.

[5] For example, see Article 61 of the Association Agreements signed between the EU and Algeria in 2002.

[6] Source: ECB (2005), Statistics Pocket Book. Table 5.3

[7] Source: ECB (2005), Statistics Pocket Book. Table 5.1

[8] Source: EU (2003); European Energy and Transport .Trends to 2030. Summary Energy Balances and Indicators. Appendix 2.

[9] Source: EU (2004); European Union Energy &Transport in Figures. 2004 edition. Table 2.2.1