The Barcelona Process, formally launched at the 1st Euro-Mediterranean Conference in 1995, was the continuation of an effort to create a common area of development and stability in the Mediterranean. Indeed, bilateral cooperation agreements had already been signed with countries in the region in the late nineteen-seventies with a view to achieving the gradual establishment of a Euro-Mediterranean free trade area by 2010. To this end, the agenda called for the gradual elimination of all barriers (tariff and non-tariff) to free trade in manufactured goods according to the timetables and talks between the different parties to the bilateral agreements, whilst the liberalisation of trade in agricultural products would be slower and more selective. The agenda also emphasised the need to reach agreements regarding rules of origin, protect intellectual property, apply European phytosanitary standards to agricultural products, eliminate technical barriers, promote competition and gradually eliminate the obstacles to direct investment.

Since the 1995 Barcelona Conference, eight Euro-Mediterranean ministerial conferences have been held. Moreover, the European Neighbourhood Policy (ENP), launched in 2004, the European Neighbourhood and Partnership Instrument (ENPI), created in 2006, the Agadir Agreement, ratified in 2006, and the Union for the Mediterranean (UfM), founded in Paris in 2008, have all provided new impetus for the process.

The ENP applies to most Mediterranean countries, as well as to some of the EU’s Eastern European neighbours. The ENP seeks to take existing relations to a new level and to deepen economic integration. In addition to liberalisation of trade in goods and services, the ENP promotes binding bilateral agreements in the spheres of economic regulation, intellectual property rights, public procurement, trade facilitation and competition. Moreover, the ENP action plans encourage countries to enter into bilateral and regional agreements that promote South-South and East-East investment and trade.

The Agadir Agreement was signed in 2004 by Tunisia, Morocco, Jordan and Egypt to establish a free trade area between them; it was ratified in 2006 and entered into force in 2007. Its objectives are quite ambitious and are geared towards achieving true regional integration of the signatory countries. However, its implementation has been delayed by several procedural problems. Moreover, for the gradual integration it envisages to occur, a stronger political commitment by the member countries and strict oversight of the agreement will be needed.

The ENPI substitutes the MEDA (Mediterranean Economic Development Area) programme that was launched in 1996 and amended in 2000. This instrument allows the EU to provide technical and financial assistance to partner countries with a view to advancing towards the creation of a free trade area.

Finally, the UfM entailed the re-launching of the Barcelona Process. It includes the 27 member states of the EU and 16 partners from the Southern Mediterranean and Middle East. It aspires to provide a new boost to Euro-Mediterranean cooperation through the execution of specific projects in a variety of spheres (the environment, regional and international transport, energy, culture, education, SMEs, etc.), which, although first provided for in 1995, have not been carried out in all this time.

In some ways, the progress made over the last nearly 15 years has been modest, despite the considerable economic resources that have been used to promote the development of regional networks and association agreements. The southern economies depend heavily on foreign trade with the EU, and yet trade flows between the EU and Southern and Eastern Mediterranean countries account for only 8% of the total and the EU is a net exporter. Moreover, the southern countries’ exports to the EU are not particularly diversified and are mainly comprised of energy, textiles and clothing and certain agricultural products subject to major restrictions. South-South regional integration is likewise negligible and trade among these countries accounts for only 6% of their total foreign trade. Furthermore, whilst the EU is the main investor in the partnership region, its direct investment there is quite low compared to its investment in other regions of the world (less than 3% of the total). Compounding matters, the partnership countries are saddled by high levels of foreign debt (although this debt has fallen in recent years) and inadequate physical and administrative infrastructure. In short, the situation on the two shores of the Mediterranean is quite asymmetrical, and not just in the economic sphere. The region thus suffers from a certain degree of instability, strong migratory flows and considerable environmental degradation.

The Current State of Economic Integration

The implementation of a Free Trade Area (FTA) increases trade-related efficiency and welfare when more efficiently produced goods and services imported from other countries in the FTA replace less efficiently produced local goods and services. However, it can also cause losses in efficiency and welfare if imports from the FTA are given preference over those of even more efficient third-party countries. To determine the net effects of integration, both effects must be taken into account. Notwithstanding the above, FTAs have other benefits. Integration tends to be accompanied by faster technological change and positive externalities between companies. As a result, it is thought to intensify economic growth.

Certain indicators shed light on the effects of the Euro-Mediterranean agreement, both with regard to integration between the EU and Southern and Eastern Mediterranean (MED) countries and with regard to integration among the MED countries themselves. In other words, they offer insight into both North-South and South-South integration.

Perhaps one of the most striking things these indicators show is the gaping disparities between different MED countries’ economic performances.

CHART 1 GDP per capita (2008)

Among the MED countries considered here, Mauritania is the poorest in terms of GDP per capita, whilst Israel is the richest. It is followed by Libya and Turkey, although the ranking changes when constant dollar GDP is taken into account, given the high inflation suffered by many countries in the region.

TABLE 1 Inflation Rate (GDP Deflator)

| Average | Average | |

| 1990-2008 | 2004-2008 | |

| Euro Zone | 3.0 | 2.5 |

| Morocco | 3.1 | 2.2 |

| Tunisia | 3.9 | 3.4 |

| Jordan | 4.2 | 6.7 |

| Israel | 7.0 | 0.9 |

| Syria | 8.9 | 12.9 |

| Egypt | 8.9 | 10.0 |

| Mauritania | 9.5 | 14.2 |

| Lebanon | 14.6 | 3.0 |

| Algeria | 16.5 | 12.3 |

| Libya | 23.2 | 25.4 |

| Turkey | 52.8 | 9.4 |

Source: World Development Indicators 2009.

Turkey and Libya have suffered, and continue to suffer, very high inflation, as do Algeria, Egypt and Syria. Morocco and Tunisia have the lowest inflation, and special attention should be called to Israel, which, in recent years, has registered an average inflation rate of less than 1%. That said, average inflation in the country over the 1990-2008 period as a whole topped 7%. Mention must also be made of Lebanon, which has seen a drop in average inflation in recent years, although the rate climbed perilously back up over 7% in 2008.

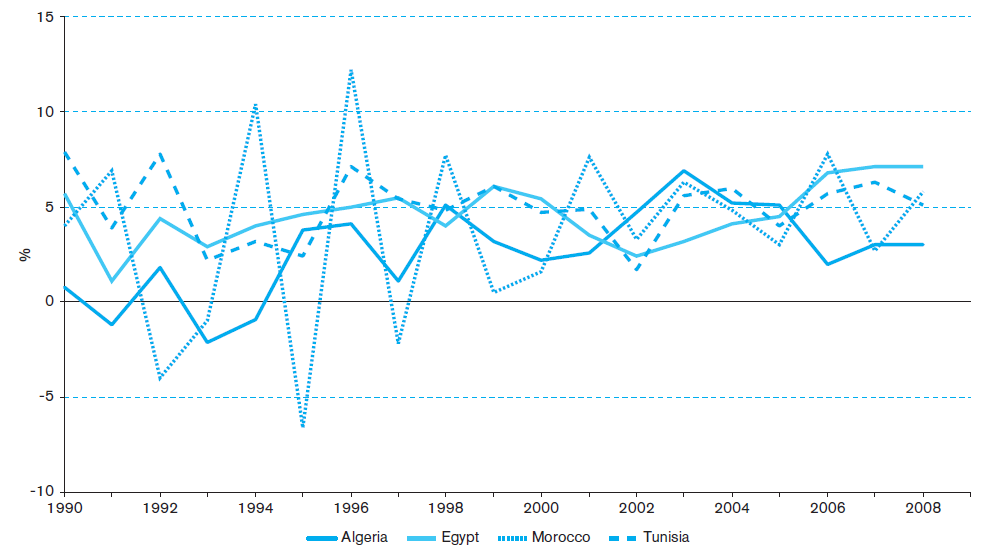

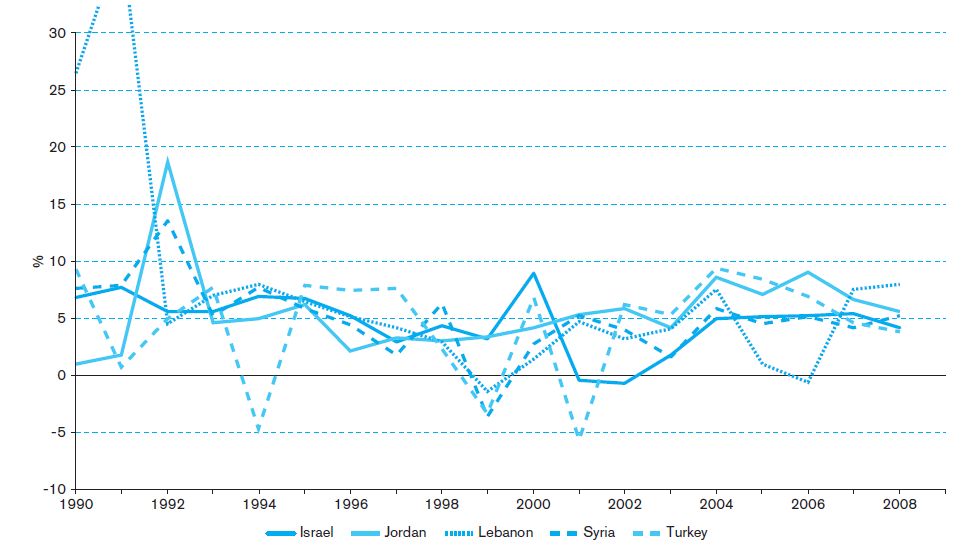

Charts 2 and 3 show the more erratic growth of Eastern Mediterranean economies as opposed to their North African counterparts. In recent years, Egypt and Tunisia have seen high and relatively stable growth rates compared to their neighbours.

CHART 2 Annual Growth in Southern Mediterranean Countries

As for the Eastern Mediterranean countries, Turkey and Lebanon stand out for their economic volatility, whilst Jordan and Syria have registered more sustained growth. Israel has also seen greater stability since 2004.

CHART 3 Annual Growth in Eastern Mediterranean Countries

Several preferential agreements have been signed in the region, and the EU, the Pan-Arab Free Trade Area (PAFTA) countries and the USA are its main trading partner. Trade relations between the EU and MED countries are governed by the Euro-Mediterranean Partnership, launched in November 1995. Partner countries include Algeria, Egypt, Israel, Jordan, Lebanon, Morocco, Syria (since December 2008), Tunisia and the Palestinian Territories, as well as Turkey. An agreement with Libya is also currently being studied. The USA has signed trade agreements with Morocco, Egypt and Jordan.

Regional alliances include, among others, the Agadir Agreement, signed by Tunisia, Egypt, Morocco and Jordan. Likewise, Egypt, Jordan, Tunisia, Syria, the Palestinian Territories, Lebanon, Libya and Morocco are members of PAFTA, and Mauritania and Algeria are currently involved in the accession process. Turkey has free trade agreements with Israel, Morocco, the Palestinian Territories, Syria, Tunisia and Egypt; it is also currently engaged in talks with Jordan and Lebanon.

This profusion of regional agreements means that a compromise must be reached to harmonise rules of origin, quality standards, phytosanitary standards and regulations in general in the different countries if greater integration is to be achieved.

North-South Integration

EU exports to MED countries accounted for 9.7% of all EU exports in 2007. Likewise, imports from MED countries accounted for about 7.5% of all EU imports. The EU primarily exports machinery, transport equipment and chemicals to MED countries (approximately 80% of all exports to these countries). Imports include fuel (22%), textiles and clothes (18.3%) and, since 2006, transport equipment, pharmaceuticals and electronics (17.5%).

From the point of view of the MED countries, the EU receives about 47% of their exports, which have registered an average annual growth of more than 10% since 1999. Thus, EU imports from MED countries have doubled over the last 10 years, with the largest increases seen in imports from the Palestinian Territories, followed by Turkey and Algeria.

EU exports to MED countries have grown at an average annual rate of 8% since the mid-1990s, registering an increase in export value of approximately 250% between 1995 and 2007. The highest average annual growth rates were seen in the Palestinian Territories, where initial levels were quite low, followed by Turkey, Morocco, Jordan, and Algeria. However, MED country exports to the EU have not grown as fast as their exports to the rest of the world. Whilst the EU is indeed the “natural” partner of many of the MED countries, and greater liberalisation would thus contribute to promoting trade between them, other countries trade heavily with the USA. This is the case with Israel and Jordan and, more recently, Morocco. Likewise, although the MED countries’ European imports have increased, so have their imports from the rest of the world. In this case, the trade liberalisation process has not led to a shift in the sources of their imports that benefits the EU.

The MED countries’ trade deficit with the EU has gradually narrowed. In the mid-1990s, the trade deficit in goods stood at more than 20% of the bilateral trade between the EU and the MED countries. More than a decade later, this deficit has fallen to 7%. Whilst this decrease can be partly explained by the trade liberalisation process with the EU and extensive structural and market reforms, attention must also be drawn to the significant increase in energy prices.

Levels of protectionism remain quite high with some exceptions. Although trade tariffs under the most-favoured nation scheme have fallen in Lebanon and Tunisia, they remain high in the latter country, as they do in Algeria,, Egypt, Mauritania, Morocco and Tunisia. Israel and Turkey have had lower tariffs for some time. Consequently, one can reasonably assume that greater trade liberalisation would have a significant impact on some of these countries.

With regard to non-tariff barriers, one hurdle is the wide array of standards used in the different MED countries, although significant progress has been made on the harmonisation of these standards with those of the EU. Nevertheless, the EU has shown a certain wariness with regard to approving the standards of MED countries, primarily due to their lack of investment in equipment and laboratories. In the sphere of health and phytosanitary standards, some MED countries have gone so far as to ban the import of certain European goods (e.g., Morocco banned the import of live cattle and derivative products, except for animals used for breeding, due to the bovine spongiform encephalopathy epidemic that has affected several mainly European countries). However, these countries encounter stumbling blocks of their own for the export of certain agricultural and livestock products to the EU. Other non-tariff barriers include import licenses (e.g., in Syria), customs duties, consular fees, requirements to use certain infrastructure or entryways, delays in the award of public tenders, anti-competitive behaviour, lack of protection of intellectual property rights and lack of transparency in public procurement.

South-South Integration

As can be seen in Table 2, the MED countries do not trade much amongst themselves. The table shows the total value of each MED country’s exports and imports (in current dollars) and each trade partner’s share of the total. Proportionally speaking, except for the Palestinian Territories, Syria and Lebanon are the region’s largest traders: 22% of Lebanese exports go to MED countries and 14% of its imports come from MED countries. The figures are similar for Syria.

Given the high level of protectionism that still exists, one might think that greater liberalisation would have a significant impact. However, a more detailed look at the data shows that the MED countries’ offer does not always meet their own demand. Consequently, the prospects for increased regional trade are not bright. This notwithstanding, in many cases these countries have similar exports, which would hypothetically allow each country to seek a high degree of specialisation within a single industry, thereby enabling subsequent trade between them. For example, one country could assemble a product whose different components are manufactured in other countries in the region. Such an arrangement might lead to a gradual increase in trade and regional integration.

TABLE 2 Trade Flows between MED Countries in 2007

| Algeria | Egypt | Israel | Jordan | Lebanon | Libya | Mauritania | Morocco | Palestinian T. | Syria | Tunisia | Turkey | Intra – MED | Total | ||

| Algeria | Imports | — | 0.9 | 0 | 0.4 | 0.1 | 0 | 0 | 0.2 | 0 | 0.1 | 0.8 | 3.3 | 5.8 | $27,631,203,951 |

| Exports | — | 0.7 | 0 | 0 | 0 | 0 | 0.1 | 1 | 0 | 0 | 0.1 | 3.4 | 5.4 | $60,163,160,346 | |

| Egypt | Imports | $26,928,845,762 | |||||||||||||

| Exports | 0.4 | 0.1 | 1.9 | 2 | 1.5 | 0.2 | 1 | 0.3 | 1.3 | 0.8 | 2.7 | 12 | $16,100,640,388 | ||

| Israel | Imports | 0 | 0.2 | — | 0.1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 2.8 | 3.1 | $56,619,379,000 |

| Exports | 0 | 0.3 | — | 0.5 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 2.2 | 3 | $54,091,395,000 | |

| Jordan | Imports | 0 | 4.4 | 1.1 | — | 0.8 | 0 | 0 | 0.2 | 0.2 | 2.7 | 0 | 2.9 | 12 | $13,531,100,490 |

| Exports | 2 | 1.4 | 2.7 | — | 2.2 | 0.6 | 0 | 0.2 | 0.9 | 4.7 | 0.3 | 0.4 | 15 | $5,700,016,552 | |

| Lebanon | Imports | 0.1 | 5.5 | 0 | 0.8 | — | 0.4 | 0 | 0.4 | 0 | 2.2 | 0.1 | 4 | 14 | $11,814,556,538 |

| Exports | 0.5 | 4.6 | 0 | 3.5 | — | 0.1 | 0.1 | 0.6 | 0 | 8.6 | 0.5 | 4.6 | 23 | $2,816,320,674 | |

| Libya | Imports | ||||||||||||||

| Exports | |||||||||||||||

| Mauritania | Imports | 0.1 | 0.7 | 0 | 0 | 0 | 0 | — | 1.5 | 0 | 0 | 0.6 | 0.4 | 3.4 | $1,430,418,276 |

| Exports | 0.3 | 0 | 0 | 0 | 0 | 0 | — | 0 | 0 | 0 | 0 | 0 | 0.3 | $1,353,710,449 | |

| Morocco | Imports | 2.5 | 1.1 | 0 | 0 | 0.1 | 0.3 | 0 | — | 0 | 0.1 | 0.6 | 2.7 | 7.4 | $31,650,391,538 |

| Exports | 0.5 | 0.3 | 0 | 0.2 | 0.2 | 0.3 | 0.3 | — | 0 | 0.3 | 0.6 | 0.9 | 3.5 | $14,607,345,568 | |

| Palestinian T. | Imports | 0 | 0.9 | 74 | 1.4 | 0 | 0 | 0 | 0 | — | 0 | 0 | 2.6 | 78 | $3,141,279,290 |

| Exports | 0.3 | 0.2 | 85 | 6.7 | 0 | 0 | 0 | 0 | — | 0 | 0 | 0.2 | 92 | $512,982,820 | |

| Syria | Imports | 0.6 | 4.4 | 0 | 1 | 1.2 | 0.8 | 0 | 0.2 | 0 | — | 0.1 | 3.9 | 12 | $14,655,130,254 |

| Exports | 2.5 | 3.8 | 0 | 4.6 | 3.2 | 1.7 | 0.1 | 1.9 | 0 | — | 0.8 | 5.2 | 24 | $11,545,710,211 | |

| Tunisia | Imports | 1.6 | 1.1 | 0 | 0.1 | 0.1 | 3.4 | 0 | 0.4 | 0 | 0.3 | — | 2.6 | 9.5 | $19,099,373,217 |

| Exports | 1.9 | 0.6 | 0 | 0 | 0 | 4.6 | 0.1 | 1.1 | 0 | 0 | — | 1.2 | 9.6 | $15,165,396,232 | |

| Turkey | Imports | 1.2 | 0.4 | 0.6 | 0 | 0.1 | 0.2 | 0 | 0.1 | 0 | 0.2 | 0.1 | — | 3.1 | $170,062,714,501 |

| Exports | 1.2 | 0.8 | 1.6 | 0.4 | 0.4 | 0.6 | 0 | 0.7 | 0 | 0.7 | 0.5 | — | 7.1 | $107,271,749,904 | |

| MED | Imports | 0.9 | 1 | 1 | 0.1 | 0.1 | 0.4 | 0 | 0.1 | 0 | 0.3 | 0.2 | 1.6 | 5.8 | $376,564,392,817 |

| Exports | 0.7 | 0.8 | 0.8 | 0.5 | 0.3 | 0.6 | 0.1 | 0.7 | 0 | 0.5 | 0.3 | 1.6 | 6.9 | $289,328,428,144 |

Source: CASE Network Report and COMTRADE.

The Potential Impact of Trade Liberalisation

Gravity models are often used to assess the impact of trade liberalisation on the trade flows between countries. These models are based on Newton’s law of gravitation and can be summarised thusly: the trade flows between countries depend (positively) on the force of attraction between them and (negatively) on the communication barriers between them. Specifically, bilateral trade between two countries depends positively on the size of their markets (often indicated by their GDP) and negatively on the distance between them. Other contributing factors are transaction costs (both monetary and non-monetary), current regional economic agreements, a common language, similar culture, trade complementarity or the lack thereof, natural resource availability, the existence of non-trade barriers, etc. Once the factors affecting current trade levels have been estimated, the model is used to calculate potential trade in a hypothetical scenario with greater liberalisation (e.g., following the elimination of all tariffs). This potential trade is then compared with actual trade.

Although most free trade agreements are relatively recent and it is therefore difficult to assess their impact on trade using available data, the research conducted to date seems to indicate that trade between the EU and MED countries has not yet reached its full potential, whilst intra-regional trade between MED countries is unlikely to increase significantly in the near future. (See, for example, Péridy, 2005a and 2005b; Nugent and Yousef, 2005; Ferragina, Giovannetti and Pascore, 2005; Ruiz and Vilarrubia, 2007; or Abedini and Péridy, 2008).

Countries such as Tunisia, Morocco and Israel are quite close to the gravity model predictions with regard to the volume of their exports to the EU-15. In contrast, Jordanian and Egyptian exports to the EU have not yet reached their potential. Part of the problem is that the EU has preferential agreements with many countries outside the MED region. Moreover, these agreements primarily focus on manufactured goods and energy products and do not address other sectors such as agriculture or services. Non-tariff trade barriers are another major problem, along with the quality, or even absence, of institutions in the MED countries (Meon and Sekkat, 2004; Kheir-El-Din and Ghoneim, 2005). Additionally, in most of these countries, infrastructure is poor, economic policy is erratic and internal political tensions are not conducive to regional trade.

A deeper integration that brought MED countries’ tariffs and non-tariff barriers into line with those of EU countries would have a ripple effect on trade between the two blocs. However, there is little hope of substantially increasing trade amongst MED countries themselves, primarily due to the low level of complementarity between their trade structures and their low GDPs. Some authors have argued that even if the trade barriers (tariff or non-tariff) were dramatically reduced, given their current GDP growth rates, MED countries would take some 40 years to reach their full trade potential with the EU.

Trade barriers (both formal and informal) are particularly important. For example, in some countries, certain goods are subject to quotas, in particular, consumer goods that compete with local goods. Additionally, the public sector has a monopoly on the import of certain goods through State-owned companies or State boards of trade. Import processes are extremely complicated due to technical inspections and customs clearance procedures. These inspections are sometimes conducted in order to ensure that imported goods comply with sanitary and safety regulations. Prior to Tunisia’s entry in the WTO, technical inspections in the country were equivalent to a tariff of 25.9%; by 2001, this burden was equivalent to a tariff of 30.5% (El-Rayyes, 2007).

Additionally, in some countries abuse by public officials can pose a barrier. Such behaviour is possible due to the lack of clear institutional standards, and it can only be eradicated by means of institutional reforms (see Kheir-El-Din, 2006, and Radwan and Reiffers, 2005). To this end, attention should be called to Morocco, whose customs reform has managed to dismantle most non-tariff barriers.

Notwithstanding the above, the possibility of increasing the volume of trade between Southern and Eastern Mediterranean countries is limited by the low absorption capacity of their markets compared to that of other markets. Some authors suggest that new avenues, such as energy cooperation or the free circulation of production factors, must be explored in order to accelerate regional integration.

The Future of Integration

At the last Euro-Mediterranean Ministerial Conference, held in Brussels in December 2009, the ministers endorsed the roadmap drafted at the Lisbon Conference in 2007. This roadmap identifies concrete actions intended to enhance economic integration and boost Euro-Mediterranean trade and investment by 2010 and considers gradually replacing the current association agreements with broader free trade agreements, in terms of both the number of member countries and the sectors covered. In particular, it requires the agreements to include agriculture and fisheries products, both of which are extremely important sectors for certain Maghreb countries.

Additionally, a mechanism must be created to facilitate both trade and investment and it must be operational by late 2010. The business world’s involvement is critical to this effort, as is strengthening institutional powers and promoting the exchange of information and experiences. Tariffs must be eliminated and replaced by agreements on different regulatory aspects, although these must take into account each country’s specific conditions and should therefore be reached bilaterally.

Regional integration amongst southern countries is key to the free trade area and will be necessary to complete the network of free trade agreements between the different countries of the south. Additionally, steps must be taken to go beyond mere trade in goods and include services, investment and regulation.

In short, there are two priority lines of action: the inclusion of measures to facilitate market access (reduction in tariffs, harmonisation of rules of origin and standards) and the creation of mechanisms to improve the competitiveness of firms from MED countries (financial and technical assistance, protection of intellectual property rights, simplification of bureaucratic and customs procedures, knowledge transfer, and greater transparency and competition in public procurement).

All of these measures are ultimately geared towards achieving a deeper type of integration, one that goes beyond mere trade liberalisation and seeks broad legislative and regulatory harmonisation, too. However, only if the plans and good intentions are brought to life in the form of actual bodies, mechanisms and tangible actions will progress be made towards the hoped-for common area of development and stability in the Mediterranean.

References

Abedini, J.; Péridy, N. “The Greater Arab Free Trade Area (GAFTA): an Estimation of Its Trade Effects.” Journal of Economic Integration, No. 23(4); pp. 848-872, 2008.

Blanc, A. “El proceso euromediterráneo: una década de luces y sombras.” Anuario de derecho internacional, No. 21, pp. 185-225, 2005.

Dennis, A. “The Impact of Regional Trade Agreements and Trade Facilitation in the MENA Region.” World Bank Policy Research Working Paper, No. 3837, Washington DC: The World Bank, 2006.

“Economic Integration in the Euro-Mediterranean Region.” Center for Social and Economic Research Network Report, No. 89, 2009.

El-Rayyes, T. “Trade and regional integration between Mediterranean partner countries.” Go-Euromed Working Paper, No. 10, 2007.

European Parliament. Resolution of 25 November 2009 on the Euro-Mediterranean economic and trade partnership ahead of the 8th Euromed Ministerial Conference on Trade.

Ferragina, A.; Giovannetti, G.; and Pascore, F. “A Tale of Parallel Integration Processes: A Gravity Analysis of EU Trade with Mediterranean and Central and Eastern European Countries,” IZA Discussion Paper, No. 1829, 2005.

Kheir-El-Din, H.; Ghoneim, A. “Arab Trade Integration in Retrospect: Comparison with the European Union Experience and Lessons Learnt.” University of Cairo, mimeograph, 2005.

Martín, I. “Asociación Euromediterránea, zonas de libre comercio y desarrollo en los países del sur del Mediterráneo,” Anuario Jurídico y Económico, No. 36, 2003.

Méon, P.G.; Sekkat, K. “Does the Quality of Institutions Limit the MENA’s Integration in the World Economy?” The World Economy, No. 27(9), pp. 1475-1498, 2004.

Nugent, J. B.; Yousef, T.M. “Does MENA Defy Gravity? How MENA Has Performed in Its Intraregional, EU and Other Trade: Implications for EU and Intra-MENA Trade Arrangements,” EUI Working Paper RSCAS, No. 26, 2005.

Péridy, N. “Towards a Pan-Arab Free Trade Area: Assessing Trade Potential Effects of the Agadir Agreement,” The Developing Economies, XLIII, No. 3, 329-345, 2005a.

Péridy, N. “Trade Prospects of the New EU Neighborhood Policy: Evidence from Hausman and Taylor’s Models,” Global Economy Journal, vol. 5, No. 1, 2005b.

Radwan, S.; Reiffers, J. “The Euromediterranean Partnership, 10 Years After Barcelona: Achievements and Perspectives,” FEMISE Report, 2005.

Ruiz, Juan M.; Vilarrubia, Josep M. “The Wise Use of Dummies in Gravity Models: Export Potentials in the Euromed Region,” Banco de España Research Paper, No. WP-0720, 2007.